Kal Ki Tayyari: night-desk read for the Fri 15 May 2026 session

Night-desk read at 22:00 IST. US handover, Asia open posture, the levels writers will defend tomorrow, and the 48-hour calendar risk.

At 22:00 IST the desk closes its notebook on a Thursday that finally gave the bulls a tape, and looks across the dateline to a Friday open that already carries a temperament. Nifty stamped a 23,689.60 close, up 1.18 percent, but the week underneath it is still red by two percent and the writers are not in a forgiving mood. June series begins tomorrow, the May contract has been buried, and the rollover residue is sitting on every strike on the chain.

US handover

Wall Street is in session as this desk publishes. The Nasdaq, the S&P 500 and the Dow are doing the overnight work that decides whether Mumbai opens with an inheritance or an obligation, and the desk is not going to print a number it has not seen settle. The frame to watch is structural, not point-precise. American tech has been a fragile partner for Mumbai's IT names this week, and the Nifty IT index closed minus 1.99 percent on Thursday even while the broader market ripped 1.18. That divergence is the tell. If the Nasdaq finds a bid overnight and closes green, the IT pack gets one session of relief and the index breadth widens at the Friday open. If the Nasdaq fades into its bell, the IT drag continues and the heavyweight basket has to do the lifting without its growth wing. A softer DXY and a 4.30 area print on the ten-year is the cocktail that lets emerging-market risk breathe. A firmer dollar and a four-three-five plus yield is the cocktail that asks for a defensive open.

Asia open posture

The 06:00 IST tape is where the desk reads the handoff. SGX Nifty premium or discount to the NSE close is the cleanest tell of overnight intent, but tonight that number has not settled and the desk will not invent one. The structural read is this. Nifty closed at 23,689.60. Above 23,700 the writers' Friday floor is in play. Below 23,500 the bears have a fresh shoulder to lean on. Whatever number the GIFT print shows at 06:00, anchor it against those two levels first.

Japan and Hong Kong are the second frame. The pan-Asia mood feeds Mumbai's heavyweight basket through commodity reads, with metal demand expectations driving the rolling read on the Nifty Metal index, which itself closed plus 2.04 percent on Thursday and led the back-half basket. If Hong Kong opens weak and the yuan drifts, that 2.04 percent metal print becomes harder to defend at the Friday open. If Asia opens neutral, the metal pack carries. FII provisional cash flow numbers on Thursday will tell the morning desk which side did the buying, and if FIIs print net buyers the heavyweights pull the index. If DIIs do the absorbing alone, the index travels but the mid-cap tape pays the price.

Pivot levels for tomorrow

The desk's frame for Friday's open sits on three anchors, two in the index and one in the financials.

Today's close at 23,689.60 sits inside an intraday range of 23,426.55 to 23,777.20 and the bulls won the back half. The 23,800 strike is the first ceiling the writers will defend tomorrow, sitting just above the day's intraday high and matching the put-call axis being rebuilt for the June series. Above 23,800 the next two call walls stack at 23,900 and 24,000. On the downside, 23,600 is the immediate cushion the bulls will sponsor, with 23,500 the deeper put floor that matches Tuesday's intraday low zone of 23,348.40 plus the cluster of pivots the desk has watched all week. Push above 23,800 and the gamma flips in favour of the bulls. Lose 23,500 and the put writers will not stand and fight. The chart is a corridor with both walls funded, and the first breach pays the trade.

BankNifty closed at 54,128.95, plus 1.26 percent on the day, reclaiming the 54,000 line that had been lost mid-week. The desk watches 54,000 as the immediate reclaim level the bulls need to hold into the Friday open. Above the close, 54,400 is where the call writers planted their flag during the week, and the OI walk shows fresh sellers stacked between 54,400 and 55,000. Below 54,000 the financials become a drag on Nifty rather than a partner, and the next downside test is the week's intraday low at 53,191.60. PSU Bank breadth carried the close more than the private heavyweights, with the Nifty PSU Bank index up 1.37 percent on Thursday, and that is a tell worth keeping. Hold 54,000 into the Friday open and the writers have to defend a tighter range than they want.

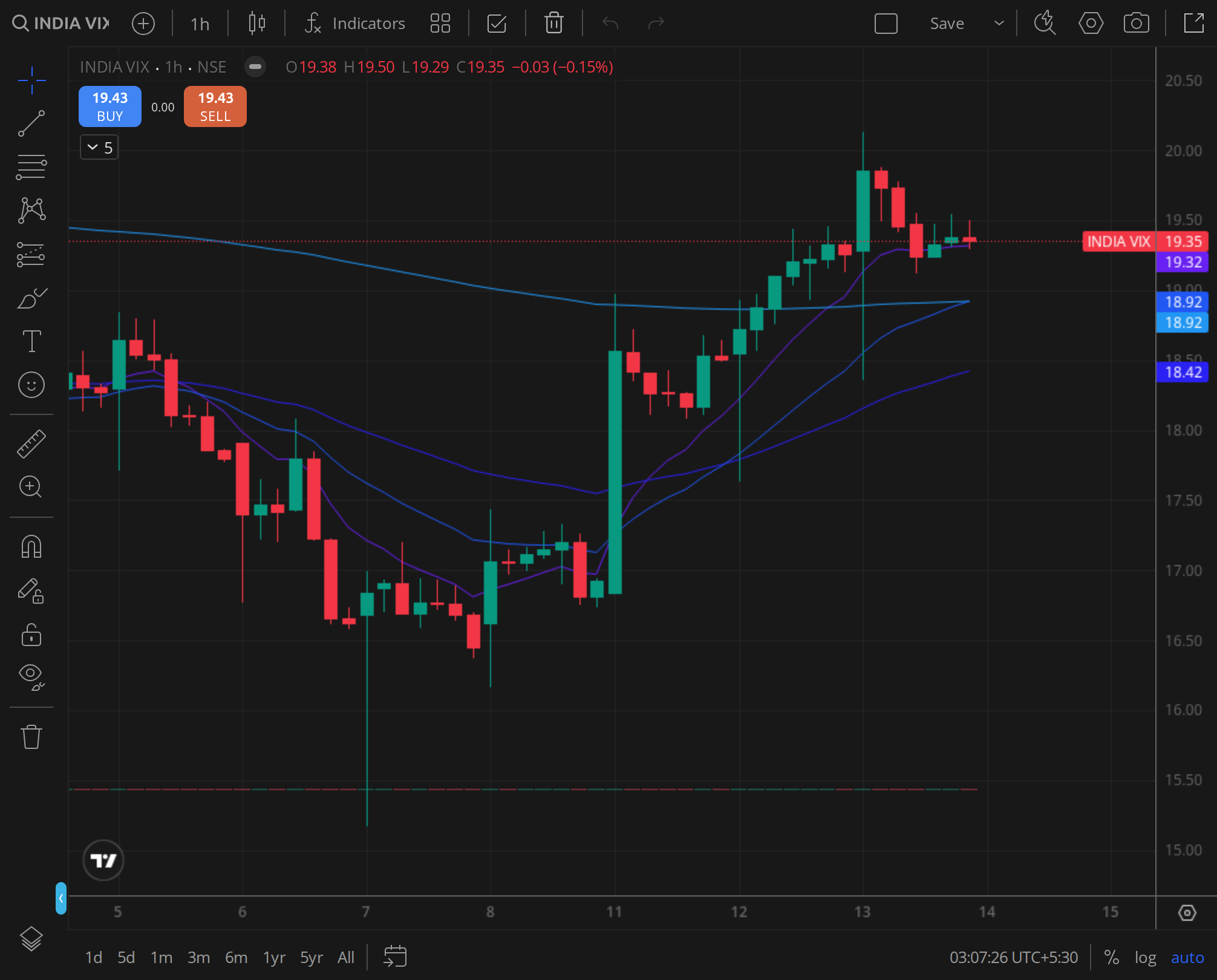

India VIX closed at 18.61, down 4.18 percent on the day, but the week's range tells a different story than the close. VIX opened the week at 16.84, ran intraday to 20.125 on Wednesday, and finished above 18 even after cooling on Thursday. That is a 10 plus percent week-on-week expansion in implied volatility, not a regime of comfort. The 18 floor is the line that decides whether premium sellers are coming back in size, and the 20 ceiling is the print that would tell the desk volatility wants more room. A close below 18 on Friday with the June series barely open is the cleanest tell that the writers are stepping back into the chain. A spike above 20 inside Friday's session, especially around a US data print, is the regime tell that strike-sellers should stand down for the week. Tomorrow's first hour is where that signal either confirms or fades.

48-hour calendar risk

The June series begins on Friday, which means every rollover desk in the city has fresh exposure to defend. Theta on the at-the-money strikes is heavy in the first session of a new series, and any unscheduled FII print can amplify the move. US data sits inside the window, with retail and inflation reads the prints that move Mumbai's overnight gap on Monday. The late-evening RBI bulletin falls inside the 48-hour frame, and the "state of the economy" chapter is the line item buy-side desks mark up first. Index heavyweight earnings continue through Friday with private banks and metals names on the docket, and the metals print can move the cyclical complex into the close, especially with the Nifty Metal index leading the Thursday tape. Crude inventories on the US side print overnight, setting Monday's OMC gap. WPI is the domestic macro print that lands inside the window.

Four things to watch in the first hour tomorrow

The desk distils the open into four reads, and they are the only four screens worth watching in the first sixty minutes.

The first is the 23,800 break. If Nifty prints above 23,800 inside the first thirty minutes and holds, the bulls have permission for a 24,000 test by midday and the call writers have to roll up. If 23,800 caps the open and the index rolls, the corridor stays the corridor.

The second is the 23,500 hold. If Nifty bends below 23,600 in the first hour and 23,500 does not buy, the bears get a fresh shoulder and the put writers will not catch the knife. The 23,348.40 print from Tuesday becomes the next live test, and the desk treats that level as the line that decides whether the week's correction is finished or whether Monday opens against another leg lower.

The third is BankNifty 54,000. If the financials hold 54,000 the index gets a partner. If 54,000 breaks the index is on its own, and the IT pack is not in a mood to help.

The fourth is the sector rotation tell. Pharma plus 2.74 percent and Metal plus 2.04 percent were the Thursday leaders, and the Friday question is whether those baskets get follow-through or whether the Thursday print was an expiry-day rotation that fades in the new series. IT minus 1.99 percent was the only major sector that closed red, and the US handover decides whether the IT drag continues or pauses. Watch the first hour's sector breadth, and the read is in your hand.

Close

The tape said yes. The chain said maybe. The week underneath said careful.

Aditya Sharma · @aditya14 · linkedin.com/in/aditya-sharma-119ab4324