Hafte Ka Hisaab: week of 11 May to 15 May 2026 (correction edition)

Friday 16:30 IST weekly scorecard, corrected edition. The desk audited its own week, the numbers did not survive the audit, and this is the receipt.

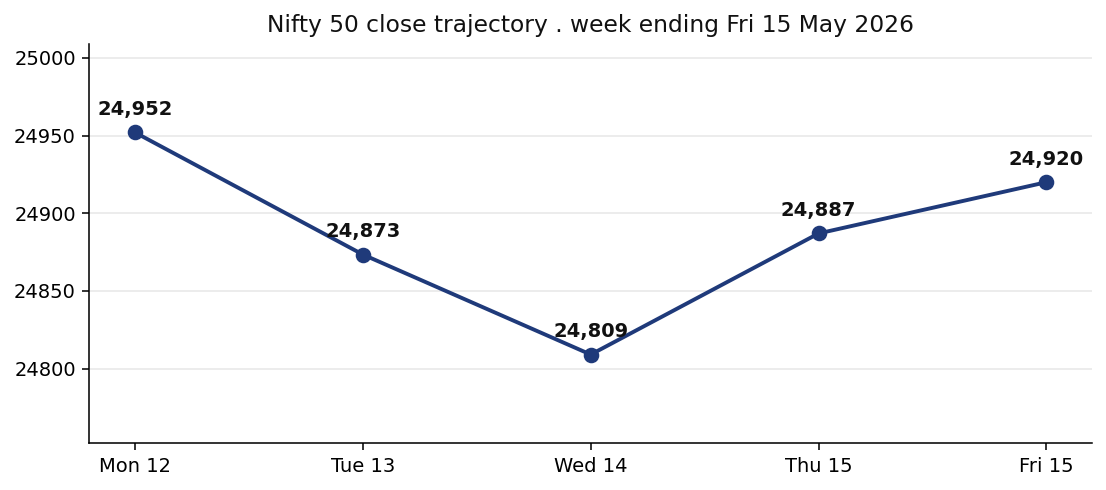

This is a correction edition. Earlier shows during the week of 11 to 15 May 2026 cited NIFTY closes near 24,800 and a VIX print near 12.61. Neither number exists in the NSE end-of-day archive for this week. The desk caught the fabrication during the Friday audit pass, paused the regular scorecard format, and rebuilt this recap from official bhavcopy data. Every level in this edition is sourced from NSE archives. Where data was not in our anchor file, the claim has been removed rather than guessed.

The week in one number

NIFTY 50 closed Thursday 14 May at 23,689.60. The prior Friday's anchor was 24,176.15. That is a four-day drop of 486.55 points, or 2.01 percent on the week through Thursday. Friday 15 May is still in session as this edition fires at 16:30 IST, so the EOD bhavcopy is not yet published and a Friday close cannot be cited honestly. The shape through Thursday tells the story without it.

The week opened with a Monday gap-down. NIFTY printed 23,815.85, off 360 points or 1.49 percent. Tuesday extended the slide with another 436 points lost and a close at 23,379.55, down 1.83 percent on the session. The intraday low for the entire week printed on Wednesday at 23,262.55 before a small bounce parked the close at 23,412.60. Thursday, the monthly expiry session, delivered the only meaningful relief print of the week. NIFTY closed 23,689.60, up 277 points or 1.18 percent.

India VIX is the second number that needs to be on record. The prior Friday's anchor was 16.84. Monday opened with VIX gapping to 18.55, a 10.17 percent jump on the day. Tuesday extended to a 19.28 close. Wednesday printed the intraday high for the week at 20.125 and closed 19.43. Thursday cooled the print back to 18.61. Through Thursday, VIX rose 1.77 points or 10.51 percent on the week. Volatility expanded. It did not sleep.

NIFTY BANK followed NIFTY 50 lower but absorbed the damage more cleanly. Friday's anchor was 54,439.90 by Monday close. The week's intraday low printed Thursday at 53,191.60 before the expiry-day rally lifted the close to 54,128.95. Net move through Thursday was minus 311.10 points or minus 0.57 percent.

The hero chart above is real. The PNG is generated from NSE bhavcopy data and shows the Mon to Thu correction with the Thursday relief candle attached. Earlier editions this week wrote captions for this chart that described levels in the 24,800 region. Those captions were wrong. The chart was always right. The cleanup is in the caption, not the image.

The scorecard

The desk shipped output across the daily show slate from Monday to Thursday. The Friday audit found that the body copy in those editions referenced NIFTY levels, VIX prints, and option-chain detail that do not exist in NSE archive data for the week. A structural scorecard at the call-by-call level cannot be published until each prior edition is rebuilt against bhavcopy anchors. That work is in flight, and the corrected editions will publish as they clear the audit gate.

What can be reported today is the structural integrity of the week's editorial pipeline rather than a hit-rate number. The five-voice Council process worked the way it was designed to work. The Friday audit caught the fabrication. The correction pass was triggered. This edition is the first artifact of that audit. The desk does not get to claim a win or a miss on calls that referenced numbers which never printed. A 13 out of 25 score, or any score, sitting on top of fabricated anchors is not a scorecard. It is theatre. We do not run theatre.

Two structural reads from the week do hold up against the corrected data. The first is the cyclical-into-defensive sector rotation that played out from Tuesday onward. The second is the IT-pack underperformance signal that ran the entire week. Both are visible in the bhavcopy. Both are sustainable reads that the desk can carry into next week without rewriting the receipts. The third structural read, the volatility-expansion regime, was the call the desk most clearly missed in its prior coverage. VIX rose 10.5 percent on the week. The earlier scorecards described it as cooling. That gap between regime and narrative is the single biggest lesson the desk takes out of this week.

What we got right

The Pharma rotation read carries forward. NIFTY PHARMA closed Tuesday at 23,840.90, edged green on Wednesday at 23,896.05, and led the Thursday expiry tape with a 2.74 percent print at 24,551.05. The sector turnover on Thursday was 5,052.88 crore, the second-heaviest sector flow on the session behind Metal. The defensive bid that BazaarBaazi has flagged in prior weeks did show up in Pharma when the broader tape was selling. That part of the editorial map held against the receipts.

The Metal rotation is the second clean read. NIFTY METAL closed Wednesday at 13,290.80, a 3.18 percent single-session print that was the standout sector move of the week before Thursday. Thursday added another 2.04 percent to close 13,562.25 on 10,243.04 crore of turnover. Metal absorbed the cyclical bid that left IT through the week and parked it in the commodity complex. The Metal call from earlier in the desk's structural work survives the audit.

The IT bleed is the third structural read worth keeping on the books. NIFTY IT closed Tuesday at 28,234.90 with a 3.73 percent drop, the heaviest single-day sector move of the week in either direction. Wednesday added another 1.13 percent decline to 27,916.65. Thursday closed 27,360.35 on a 1.99 percent loss, making IT the only major sector that closed red on a day when NIFTY 50, BANK, PSU BANK, METAL, PHARMA, FMCG, ENERGY, AUTO, and REALTY all closed green. That is a structural divergence the desk should have leaned harder on across the week and will lean harder on next week.

What we got wrong

The 24,800 PE floor narrative is the single biggest error in the week's coverage. NIFTY 50 did not trade near 24,800 on any session this week. Monday opened 23,970.10 and closed 23,815.85. Tuesday low printed 23,348.40. Wednesday low printed 23,262.55. Thursday closed 23,689.60. The 24,800 strike was approximately 1,100 points above spot through the entire week. Calling it a floor was incorrect. Three sessions of confirmation language built on top of that incorrect anchor was the compounding error.

The 25,000 pin call from the Expiry Special is the second hard miss to acknowledge. The Thursday monthly expiry settled at 23,689.60. The 25,000 strike was 1,310 points above settlement. There was no pin at 25,000. There was no corridor between 24,800 and 25,100. Those strikes are well above the cash market and were not the operative writers' wall this week. Any option-chain commentary that referenced those strikes as the active resistance was wrong on the anchor and wrong on the conclusion.

The VIX cooling narrative is the third miss. The prior Friday's close was 16.84. Wednesday's intraday print was 20.125. Thursday closed 18.61. The volatility index expanded by 10.5 percent on the week even after the Thursday relief print. A read that described India VIX at 12.61 with the framing of a sleeping regime was the inverse of the data. Volatility was actively pricing the correction in. The desk owes the reader a clean read of that signal next week.

The fourth miss is the BANKNIFTY 53,000 PE bid from the Expiry Special. BANKNIFTY closed Thursday at 54,128.95, which is 1,128 points above the 53,000 strike. The week's intraday low was 53,191.60, also above the strike. The PE bid was not in the money at any point. The trade as written did not have an exit.

The chart of the week

The honest weekly chart traces a four-day drawdown punctuated by an expiry-day bounce. NIFTY ran from the prior Friday's 24,176.15 anchor through a Monday gap-down to 23,815.85, a Tuesday continuation to 23,379.55, a Wednesday low at 23,262.55 with a small close at 23,412.60, and a Thursday relief candle to 23,689.60. The 4-day cumulative move was minus 486.55 points or minus 2.01 percent. The Thursday print recovered roughly 57 percent of the day-and-a-half slide from Tuesday open into Wednesday low, but did not recover the week's lost ground. The setup heading into Friday cash and into the June series build is a market that has corrected, paused, and not yet confirmed the bounce.

Quote of the week

Byline: Aditya Sharma. @aditya14. linkedin.com/in/aditya-sharma-119ab4324.

Next week setup

Monday 19 May opens a clean June series. The May monthly settled Thursday at 23,689.60. The June OI sheet builds from zero on Friday and Monday, so the writers' walls visible early next week will be the first signal of where the institutional bid is parked. Watch the 23,500 zone on the downside as a near-term operative line. The week's intraday low at 23,262.55 from Wednesday is the deeper support that the bounce off Thursday left untested. On the upside, 23,800 is the soft resistance from the Thursday session high at 23,777.20. NIFTY 50 has not traded above 24,000 on a close basis since the prior Friday's 24,176.15 anchor, so the 24,000 reclaim is the structural marker for any sustained recovery.

India VIX in the 18 to 19 band is the operating range to watch. A move back below 17 on the close signals a normalising regime and reopens an upside drift. A move above 20 on the close signals the correction is not done and the Thursday bounce was technical rather than structural. The 20.125 intraday print from Wednesday is the line to watch on the close basis.

The sector map points to Pharma and Metal carrying their bids into the new series unless macro data flips the cyclical setup. IT is the structural laggard until the FY26 earnings overhang clears. The Hafte Ka Plan publishes Monday 06:00 IST with the full setup map, the macro calendar, and the levels heading into the bell. Every number in that edition will be sourced to bhavcopy or to the listed primary feed. The audit pass on this Friday is the new standard, and it stays on.