Sectoral Pulse: mid-session rotation read for Thu 14 May 2026

Pharma and Metal led the rotation, IT bled a third straight session, and the cyclical recovery finally showed up after two days of selling.

The picks

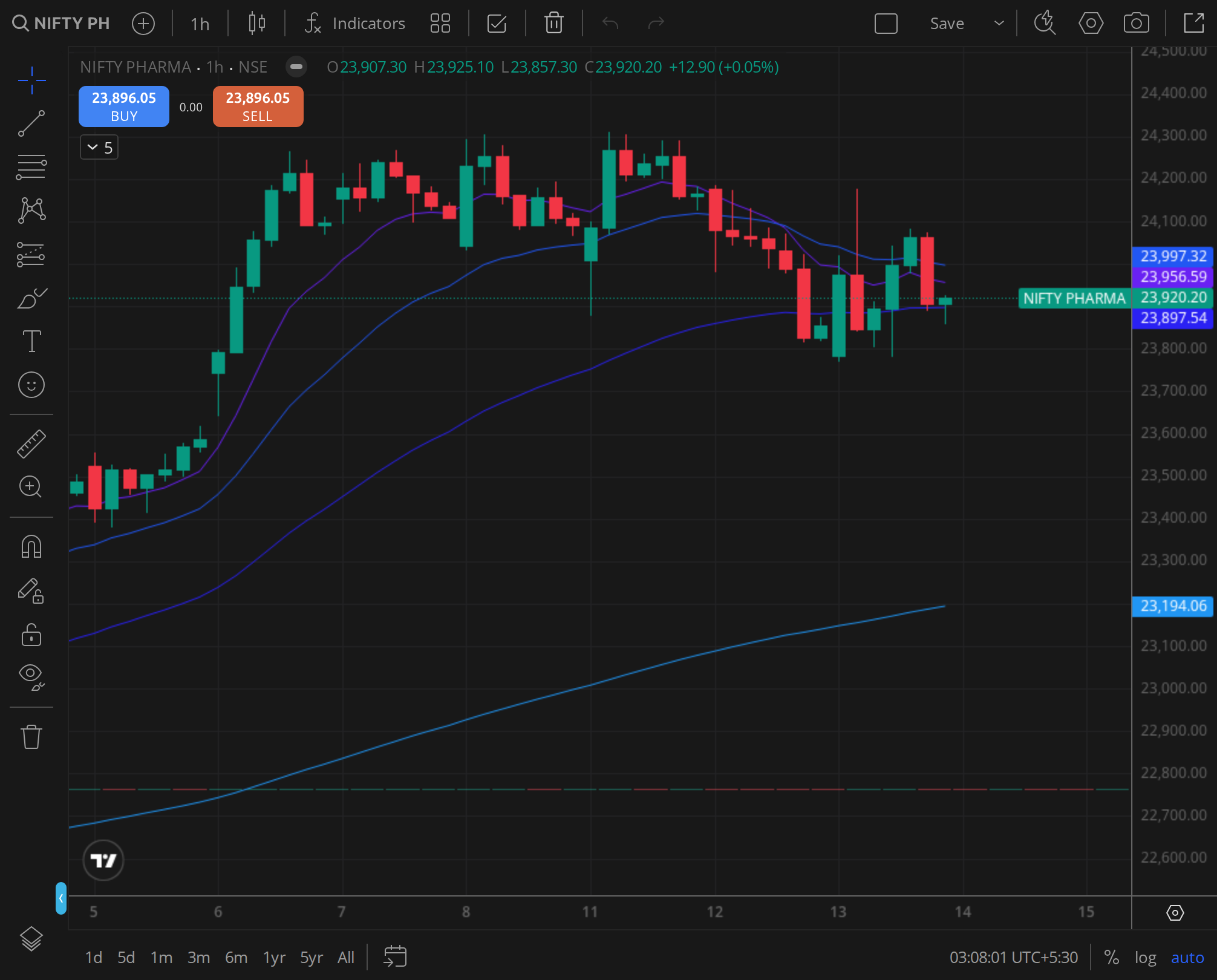

- 01NIFTY PHARMAintraday · high

Sector leader of the day with a 2.74 percent close, accelerating off Wednesday's plus 0.23 percent base after Tuesday's minus 1.36 percent flush. Defensive bid turned aggressive.

Level: Hold above the morning shelf into close · Invalidation: Reversal back below Wednesday's close

- 02NIFTY METALintraday · high

Second consecutive strong session at plus 2.04 percent on top of Wednesday's plus 3.18 percent. The cyclical bid is no longer a one-day fluke; it is a two-session trend.

Level: Sustain above the Wednesday close · Invalidation: Close back into Tuesday's range

- 03NIFTY PSU BANKintraday · medium

Plus 1.37 percent close, following NIFTY BANK's plus 1.26 percent expiry-day relief bounce. PSU credit recovered the Monday and Tuesday flush in a single session.

Level: Hold above 8,150 · Invalidation: Lose the 8,071 Tuesday base

- 04NIFTY ITintraday · medium

Minus 1.99 percent close, the only major sector in the red. Third consecutive distribution session after Tuesday's minus 3.73 percent rout. The bleed has its own rhythm now.

Level: Failure to reclaim the morning open · Invalidation: Close above 27,916 (Wednesday close) on volume

The morning tape handed leadership to Pharma and Metal while IT bled a third straight session, and the sector rotation map was the cleaner story than the headline index.

The morning rotation in numbers

Between 09:15 and 11:30, the NIFTY 50 was building what would close as a plus 1.18 percent session at 23,689.60, recovering 277 points after two punishing days that had carved the index from 24,176 (last Friday's base) down to 23,379 on Tuesday. Under the bonnet the rotation was loud and directional. Pharma was running near plus 2 percent by the second hour. Metal was adding close to plus 1.5 percent on top of Wednesday's huge plus 3.18 percent leg. PSU Bank was leading the financial pack. The leadership fingerprint was not the one the consensus desk read had penciled in for expiry day: this was defensive-plus-cyclical rotation, not export-led relief.

The fade was just as clean. NIFTY IT shed roughly 1.5 percent through the morning and held the loss into lunch, struggling to even hold its Wednesday close of 27,916. FMCG drifted around the flatline as staples took the morning off. Auto looked tucked and tentative through the first ninety minutes. The advance-decline tilt was clearly positive, but the breadth was telling you something subtler than a relief rally. This was a rotation, not a stampede.

What the tape refused to do, for the third session in a row, was give IT a single relief candle. Every bounce attempt into 11:00 was sold within minutes. By the time the bell rang Pharma had closed plus 2.74 percent at 24,551.05, Metal plus 2.04 percent at 13,562.25, and IT minus 1.99 percent at 27,360.35. The morning read was a forecast and the close was the receipt.

The week's macro context

To understand why Thursday's rotation matters, you need the week in one frame. NIFTY 50 went minus 1.49 percent on Monday, minus 1.83 percent on Tuesday, a tiny plus 0.14 percent on Wednesday, and then plus 1.18 percent on Thursday. India VIX climbed from 16.84 last Friday to 20.125 intraday on Wednesday before cooling to 18.61. The week through expiry day was minus 2.01 percent on the headline index. This is a correcting week, not a sleepy one.

That context changes the read on Thursday's sector map. The morning was not just an expiry-day relief bounce. It was the first session of the week where the cyclical book finally caught a bid, where Pharma stopped being a parking lot and started leading, and where IT continued to be the funding source for everything else. The rotation was risk-off defensive into cyclical recovery, and the leadership was wide enough to be structural rather than mechanical.

Sector by sector

NIFTY IT closed at 27,360.35, down 1.99 percent on the session and the only major sector that printed red on the screen. The index had already lost 3.73 percent on Tuesday and another 1.13 percent on Wednesday, so this was the third consecutive distribution session, not an isolated weak print. The export bench has now bled close to 6.6 percent across three sessions while the rest of the market was finding its feet. The morning rejections at the 5-day VWAP came on heavier volume than the bounce attempts, and the 50-day moving average that was acting as support through April is now overhead. The major constituents from the top of the index, the kind of names that anchor every diversified domestic equity book, were dragging rather than absorbing. The sector-level damage was distributed and not driven by a single outlier. Until IT prints a session that closes above its prior day high on confirming volume, every rally is a trim opportunity for funds that are already light here. The export catalyst the bulls need is not on the calendar this week.

NIFTY PHARMA closed at 24,551.05, up 2.74 percent and the unambiguous sector leader of the day. The setup deserves a longer look because of how cleanly it inverted across the week. Pharma was minus 1.36 percent on Tuesday alongside the broader flush, then printed a quiet plus 0.23 percent on Wednesday while the rest of the market was still finding the floor. That Wednesday base was the tell. On Thursday it accelerated into outright leadership, adding more on a single session than the headline index gained in a week. This is not just a defensive bid; this is allocators rotating real capital out of the cyclical export book and into the domestic-pricing healthcare names with a margin tailwind. The chart now sits comfortably above its 20-day moving average and the breadth inside the sector was wide rather than concentrated. The risk for chasers is mechanical. Sectors that lead the index by more than 1.5 percent on a session frequently consolidate the next morning before extending, and the close above 24,500 sets up that decision point cleanly.

NIFTY METAL closed at 13,562.25, up 2.04 percent on Thursday on top of Wednesday's enormous plus 3.18 percent print. Two consecutive sessions of strong gains, after Tuesday's mild minus 0.35 percent that had barely participated in the broader sell-off, makes Metal the cleanest two-day leader on the screen. The sector has added close to 5.3 percent across Wednesday and Thursday combined, far more than the NIFTY 50's net gain across the same window. The chart cleared its 5-day high, took out the late-April swing pivot, and now sits within reach of its 52-week zone. Volume confirmed the bid on both legs, which is the difference between a chase candle and a leadership candle. The risk here is overnight. A single hostile print on the London Metal Exchange and the crowded longs get punished into Friday's open. For now, the base-metal cyclical bid is leading the screen and the leadership is wide enough that no single stock is carrying the index.

NIFTY BANK closed at 54,128.95, up 1.26 percent on Thursday. The context matters more than the move. Banks had lost 1.57 percent on Monday and another 1.63 percent on Tuesday, a combined minus 3.2 percent over two sessions, before Wednesday's minus 0.18 percent print stopped the bleeding. Thursday's recovery took back roughly 40 percent of the Monday-Tuesday damage but left the week net negative at minus 0.57 percent through Thursday. This is a recovery, not a breakout. The morning bid was led by the cyclical-credit side of the book rather than the high-quality private-bank cohort, and the volume profile was constructive rather than spectacular. Heading into Friday, BankNifty's job is to hold above 54,000; lose that and the bounce gets retraced fast.

NIFTY PSU BANK closed at 8,174.40, up 1.37 percent on Thursday and the second-strongest mover inside the financial complex. The two-day arithmetic is telling. The sector was minus 1.10 percent on Tuesday during the broad flush, then recovered most of that on Thursday alone, putting the week-to-date hit at less than a percent through expiry day. The setup is now interesting rather than crowded. PSU credit has been the cleanest beneficiary of the rate-cycle and credit-growth thesis through April, and Thursday's session quietly confirmed that allocators are not abandoning that view despite the week's broader selling. The chart sits above its 20-day moving average, the 8,071 Tuesday low is now the line in the sand, and a close above the 8,200 zone over the next two sessions opens the next leg cleanly. The leadership inside PSU Bank was broad, with the larger constituents leading the smaller ones.

NIFTY AUTO closed at 26,049.70, up 0.62 percent on Thursday. The number understates what was actually a participation move rather than a leadership move. Auto had been minus 2.28 percent on Tuesday during the flush, then another minus 0.97 percent on Wednesday, putting the sector down close to 3.25 percent across two sessions before Thursday's modest bounce. The Thursday close is still well below Monday's open and the sector sits in the middle of the week's range, not the top of it. The chart is tucked under a clean resistance shelf from late April and the 20-day moving average is now overhead. Two-wheeler names did most of the lifting; four-wheeler heavyweights were tentative. The setup is coiled, not committed. A close above 26,200 over the next two sessions reopens the trend; a fade back to 25,900 keeps the sector in the consolidation it has worn for most of May.

NIFTY FMCG closed at 50,779.15, up just 0.34 percent on Thursday, the weakest of the green sectors and the one that says the most about how this rotation actually worked. On a day when the headline index was plus 1.18 percent and Pharma was plus 2.74 percent, staples did not participate. They got funded. The capital that should have rotated into FMCG as the textbook defensive bid instead skipped past it and went into Pharma, which behaved like a defensive with a margin catalyst attached. On a relative basis FMCG is doing its defensive job against the NIFTY 50 being down 2 percent through Thursday. The absolute read is less flattering. Staples are not going to lead anything in this regime. Volume stayed thin, so this is not distribution but neglect.

NIFTY ENERGY closed at 40,080.15, up 0.65 percent on Thursday, sitting squarely in the mid-pack. Energy did not lead and did not lag; it joined. The internal mix was telling. Power utilities did the lifting while integrated-oil names dragged. The sector turnover of just over 15,500 crore was the highest among all the sector indices, telling you that whatever rotation was happening at the index level was being expressed through energy stocks in real money terms. The sector has not picked a side for seven sessions. Until it does, this is a stock-picker's index, not a thesis trade. The close-print to watch on Friday is whether the utilities bid holds without the oil drag.

NIFTY REALTY closed at 770.10, up 0.77 percent on Thursday. The sector had been one of the cleaner relative performers through the week and the Thursday gain was the third small higher close in a row. The chart shows a textbook stair-step structure where each pullback has been shallower than the last, exactly the geometry you want in a sector acting as a rate-cycle proxy. The risk for Realty is not direction; it is overheat. The sector has extended for three sessions on tight ranges, the breakout pivot from late April is below, and any close above the recent intraday high opens the next leg on momentum alone. Inside the sector, the leadership was concentrated in the larger constituents, the cleaner kind of participation for a trend that needs to defend itself against an exhaustion print.

The synthesis

The story Thursday's screen told was not the one the consensus had penciled in for expiry day. The expected playbook was a relief bounce led by the export bench finally catching a bid, with the index pinning near a flat-to-positive close on theta mechanics. What actually happened was a wide, allocator-led sector rotation that took Pharma and Metal into leadership while IT continued the bleed for a third consecutive session.

The rotation map reads risk-off defensive into cyclical recovery. Pharma at plus 2.74 percent is the defensive bid with a catalyst. Metal at plus 2.04 percent is the cyclical bid with continuation from Wednesday's plus 3.18 percent. PSU Bank at plus 1.37 percent and NIFTY BANK at plus 1.26 percent are the credit-cycle recoveries from the Monday-Tuesday damage. Auto, Realty, Energy and FMCG are participants, not leaders. IT at minus 1.99 percent is the funding source for all of it.

The signal for the rest of the week is that this is not the sleepy DII-bid sideways tape one section of the desk read had been pricing. This is an active sector rotation inside a week that is still net negative at minus 2.01 percent through Thursday. The leadership reshuffle is real. The IT weakness is structural for now and not a one-session reaction. The cyclical bid in Metal has earned two sessions of confirmation. The Pharma move needs Friday to confirm the Thursday surge was not a single-day catch-up trade.

Aditya Sharma · @aditya14 · linkedin.com/in/aditya-sharma-119ab4324