Pratham Khabar: overnight handover and the Thu 14 May 2026 day frame

Sunrise read on the overnight tape, GIFT NIFTY positioning watch, FII carry-over read, and the signed bias for the cash open after a 2 percent two-day drawdown.

Dalal Street walks into expiry-Thursday 2026-05-14 nursing a 2 percent week-to-date drawdown, a VIX that has popped 15 percent in three sessions, and an IT pack that just lost almost 5 percent in two days. Wednesday paused the bleed at 23,412. Today is the day the tape either confirms the pause or turns it back into a slide.

Where the cash close left us

NIFTY 50 closed Wednesday at 23,412.60, up just 33.05 points or 0.14 percent, with an intraday range of 23,262.55 to 23,582.95 (NSE close 2026-05-13). That print is the soft pause in the middle of a hard correction. Monday cut the index 360 points, Tuesday cut another 436, and Wednesday gave back only the tiniest sliver of green. Week-to-date through Wednesday close, NIFTY 50 is down 763 points or 3.16 percent from Friday's 24,176.15 base, with intraday low of 23,262.55 marking the line the bulls cannot afford to lose.

NIFTY BANK closed Wednesday at 53,456.15, down 99.05 points or 0.18 percent, lagging the headline by 32 basis points (NSE close 2026-05-13). The financial pack carried a wider 909-point intraday range, swinging from 53,194.25 to 54,103.90, with sellers winning the close. Week-to-date Bank NIFTY is down 1,376 points from Friday's 54,832 open, or roughly 2.5 percent, and the 53,194 intraday low sits as the line that decides whether financials lead the relief bid or extend the slide today.

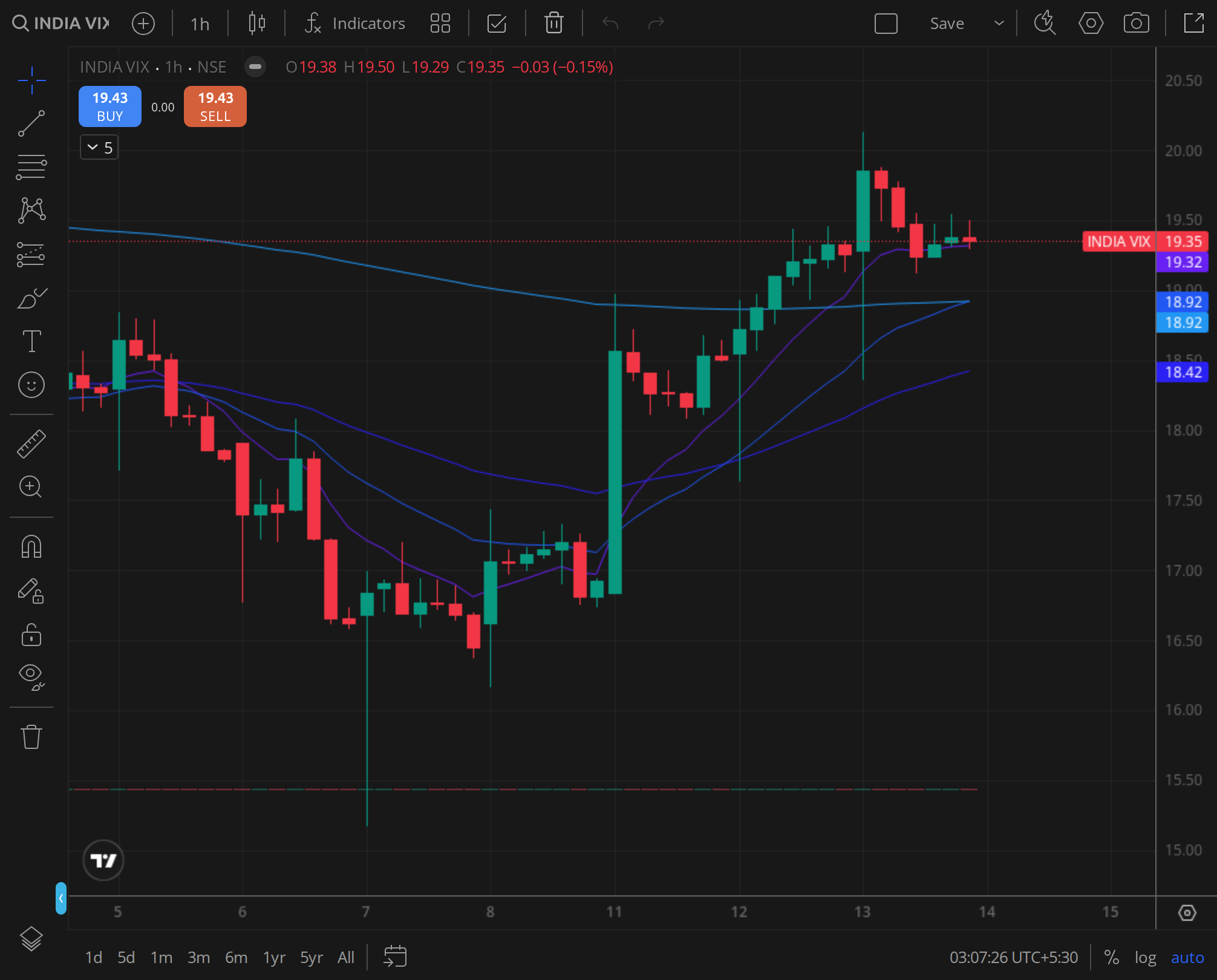

INDIA VIX closed Wednesday at 19.43, up 0.15 points on the session and printing an intraday high of 20.13 (NSE close 2026-05-13). That is not a sleepy volatility regime. Friday's base was 16.84. The week's VIX move is plus 15.4 percent through Wednesday close, with a single intraday print above 20. Premium sellers who came into Monday writing the strike are wearing the move. Premium buyers who held overnight straddles into Tuesday's 1.83 percent drop got paid. Expiry-day VIX above 19 means option pricing carries a fear bid the cash market has not yet fully respected.

The sector tape is the part the headline NIFTY does not tell. NIFTY IT closed Wednesday at 27,916.65, down 1.13 percent and extending the previous session's 3.73 percent rout (NSE close 2026-05-13). Two-day damage in IT is roughly 4.8 percent. That is the cleanest sectoral bleed on the screen, and post-FY26 earnings overhang is doing the work. NIFTY METAL closed at 13,290.80, up 3.18 percent and printing the only big-green sector card of Wednesday's session, snapping back hard from Tuesday's mild dip. NIFTY PHARMA at 23,896.05 held a small green print of 0.23 percent, the defensive bid quietly accumulating.

NIFTY AUTO at 25,888.95 closed down 0.97 percent on Wednesday after Tuesday's 2.28 percent cut, and NIFTY PSU BANK at 8,071.35 sat at down 1.10 percent week-to-Tuesday before Wednesday's relief. The sectoral picture says capital is rotating out of IT and Auto, hiding in Pharma, and chasing the Metal bounce on the back of a softer dollar tape overseas. None of this rotation has cracked the broader correction yet.

Overnight tape and GIFT NIFTY watch

The US tape closed the prior session firmer than the previous evening, which is a constructive carry-over but not a green-light gap. The desk read this morning is that Wall Street did the job of stabilising sentiment without printing an Indian-tape-rescue rally. GIFT NIFTY premium watch into the cash open is the single most important pre-market read for today, and the discipline is to wait for the 08:45 IST quote rather than front-run a number. Soft premium into the open keeps the gap polite. Steep discount flips the day frame to defensive before the bell rings.

Asia opens this morning will set the tone Dalal Street trades into 09:15. The pattern through the week has been Asian green not translating into Indian green because the domestic drag, IT earnings overhang and FII selling, has been heavier than the overnight handoff suggests. Until that delta closes, the morning template stays sceptical even on a green-Asia print.

FII and DII read

The desk read elevated FII selling pressure across Monday and Tuesday, the kind of pressure that two minus-1.5-percent and minus-1.8-percent sessions can only generate from foreign cash exits in size. Wednesday's flat tape suggests that flow either eased or got absorbed by domestic counters. DII desks have been on the bid, which is the only reason Wednesday closed green at all. The hand-on-the-tiller question for today is whether FII selling resumes on expiry-Thursday, with index futures unwind providing the second leg of any cash-side pressure.

Provisional flow numbers from NSDL and the exchange publish around 19:00 IST. Wait for the print rather than fabricate a figure pre-open.

The expiry-day calendar

Today is monthly F&O expiry. That is the single biggest structural event of the session. With NIFTY 50 sitting 763 points below Friday's open and VIX above 19, the option chain is carrying real fear premium into settlement. Strikes that were the floor on Friday are now overhead resistance, and the writers who fought the slide on Monday and Tuesday are deep underwater. Expiry mechanics tonight could produce either a relief squeeze if shorts cover or a final liquidation if hedges get monetised.

Earnings tonight after market hours bring the next macro lever. The IT pack is still digesting FY26 commentary that drove the sector down almost 5 percent in two days, and any after-hours print from a large-cap that confirms the slowdown narrative compounds Friday's open. India CPI prints later in the week, and US rate-path commentary continues to colour the dollar tape, but expiry settlement is the only thing that matters for the next nine hours.

Day frame

The dashboard does not read green. NIFTY 50 is at 23,412 after a 763-point week-to-date drawdown. VIX is at 19.43 with one print above 20 in living memory of three days. IT has lost 4.8 percent in two sessions. The 23,262 intraday low from Wednesday is the line that decides whether expiry settles with a relief bid or a final flush. Above that line and the day can grind back toward 23,580, the Wednesday intraday high. Below it, the writers who tried to hold the strike on Monday lose the floor and the cash desk has to find a new one.

Aditya Sharma · @aditya14 · linkedin.com/in/aditya-sharma-119ab4324