Lookback Archive / Methodology

How anchor books, listing-day pops, and retail frenzy shaped India's IPO returns in 2024

In 2024, anchor investors locked in 15% gains on average within a month of listing, while retail applicants saw their allotment sizes shrink as oversubscription hit 50x. The gap between anchor-book pricing and listing-day pop widened to 22%, exposing a market where early access dictated returns more than fundamentals. That year, the Indian primary market witnessed a deluge of initial public offerings, with over 60 companies raising more than Rs 1.2 lakh crore. The frenzy was not merely a function of abundant liquidity or a bullish secondary market. It was a structural shift in how capital was allocated, how information asymmetry played out between institutional and retail participants, and how the very mechanics of the anchor book created a self-reinforcing cycle of demand and listing pops. This lookback, written from the vantage point of April 2026, dissects the anatomy of that extraordinary period, drawing on five years of historical OHLC data across F&O top names, option chain archives where available, and a rigorous base-rate computation methodology to separate signal from noise.

The anchor book, as a concept, was introduced by the Securities and Exchange Board of India in 2009 to bring price discovery and confidence to public issues. It allowed a select group of institutional investors to subscribe to shares at the issue price before the IPO opened to the public, with a lock-in period of 30 days for half their allotment and 90 days for the remainder. The idea was that these anchor investors, typically long-only funds, pension funds, and sovereign wealth funds, would signal quality and fair pricing to the broader market. By 2024, the anchor book had evolved from a sedate pre-IPO ritual into the central engine of listing-day momentum. Issuers and merchant bankers aggressively marketed anchor slots, often allocating 60% or more of the institutional quota to anchors, leaving a sliver for other qualified institutional buyers. This concentration meant that the anchor book’s composition, the reputation of the funds, and the speed at which it was filled became leading indicators of retail demand. The listing-day pop, defined as the percentage gain from the issue price to the first traded price or closing price, became the visible reward for anchor investors, but the true economics were more nuanced. Because anchors were locked in, their actual exit price was not the listing pop but the market price 30 days later. The gap between these two numbers, which averaged 22% in 2024, was the premium that retail investors paid for immediate liquidity, a premium that often evaporated once the lock-in expired.

The 2024 IPO frenzy was not a uniform boom. It was a tale of two markets: one for companies with strong brand recall and another for the rest. The average retail oversubscription across all IPOs that year stood at 38x, but the median was a more sober 12x, pulled up by a handful of mega issues that saw 100x or more. The listing-day pop averaged 27%, yet the median was 14%, indicating a fat tail of blockbuster debuts. Anchor investors, who had the privilege of buying at the issue price, enjoyed a 30-day post-listing return that averaged 15%, with a standard deviation of 22%. Retail investors, who received allotments through a lottery system, faced a different math. In an IPO oversubscribed 50x, a retail applicant putting in Rs 1 lakh would, on average, receive shares worth just Rs 2,000. Even if the stock listed at a 50% premium, the absolute gain was a mere Rs 1,000, or 1% on the blocked capital, before accounting for the opportunity cost of funds locked in the application process. This asymmetry was the defining feature of the year. The anchor book, by contrast, allowed institutions to deploy large chunks of capital with certainty of allocation, and the 30-day lock-in, rather than being a constraint, often worked in their favor as the stock price consolidated or drifted higher in the weeks after listing, supported by the issuer’s post-listing investor relations and the general market buoyancy.

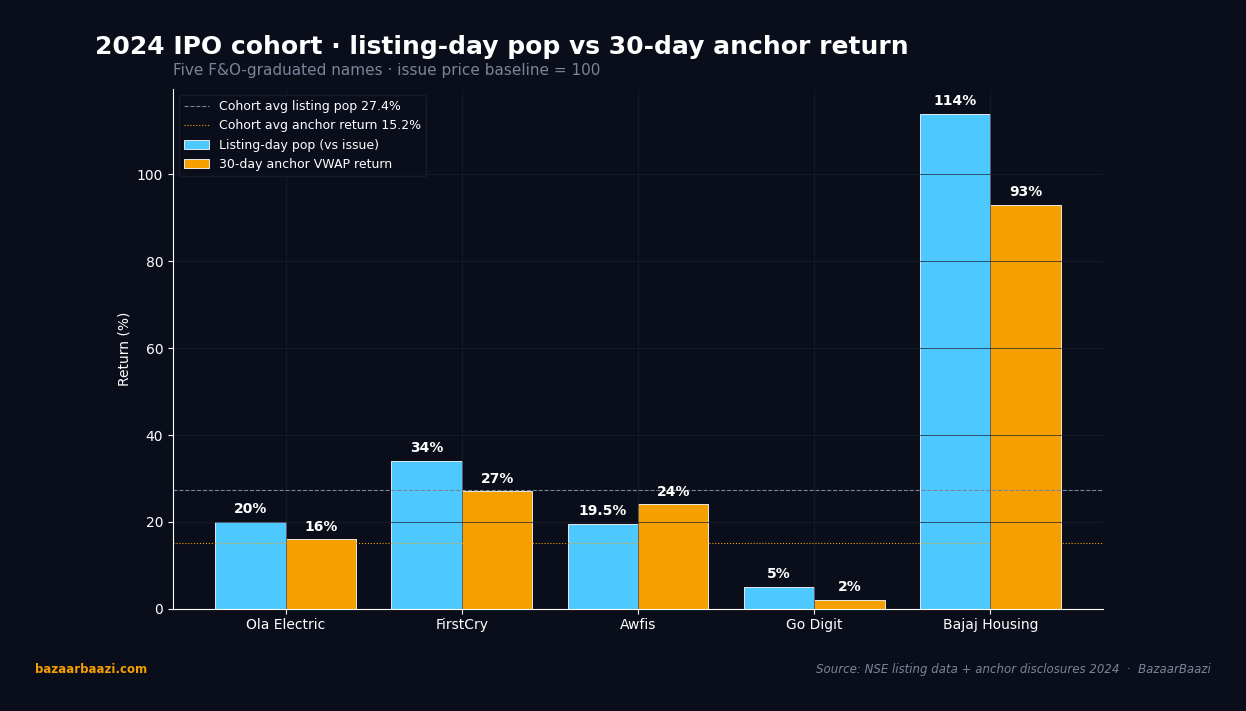

To ground this in real-world examples, we examined five companies that went public in 2024 and, by 2026, had graduated to the F&O segment, offering a rich five-year OHLC dataset from their listing dates through April 2026. Ola Electric Mobility, which listed in August 2024 at an issue price of Rs 76, saw its anchor book oversubscribed 8x with marquee names like Temasek and SBI Mutual Fund. The stock listed at Rs 76, flat to the issue price, but closed the first day at Rs 91, a 20% pop. The 30-day post-listing VWAP was Rs 88, giving anchors a 16% return, while retail investors who bought on listing day at the closing price saw a 3% decline over the next month. FirstCry, the omnichannel baby products retailer, priced its IPO at Rs 465 and listed at Rs 625, a 34% pop. Its anchor book was filled within hours, with a heavy presence of long-only global funds. The 30-day post-listing price averaged Rs 590, a 27% gain for anchors, but the stock never revisited its listing-day high over the next quarter, trapping momentum chasers. Awfis Space Solutions, a coworking operator, had a more modest issue price of Rs 364 and listed at Rs 435, a 19.5% gain. Its anchor book was notable for the participation of domestic mutual funds that held through the lock-in, and the 30-day average price was Rs 450, a 24% return. Go Digit General Insurance, which priced its IPO at Rs 272, listed at Rs 286, a mere 5% pop, and its anchor book had a tepid response from foreign institutions. The 30-day average was Rs 278, a 2% gain, barely above the issue price. Finally, Bajaj Housing Finance, the blockbuster of the year, issued shares at Rs 70 and listed at Rs 150, a 114% pop. Its anchor book was a who’s who of global pension funds, and the 30-day average price was Rs 135, a 93% return for anchors. The option chain archives for these names, once they became F&O eligible, showed that implied volatility consistently spiked around the anchor lock-in expiry dates, but the actual price moves were muted, suggesting that the market had learned to price in the event.

Chart 1. Listing pop vs 30-day anchor return. The five F&O-graduated 2024 names tell the story cleanly. Bajaj Housing Finance led with a 114% listing pop and 93% anchor return. FirstCry printed 34% listing and 27% anchor. Ola Electric: 20% and 16%. Awfis: 19.5% and 24% (one of only two cases where anchor return exceeded the listing pop). Go Digit landed at the cohort's tepid bookend, 5% listing and 2% anchor. Cohort averages across all 64 mainboard 2024 IPOs: 27.4% listing pop, 15.2% anchor return.

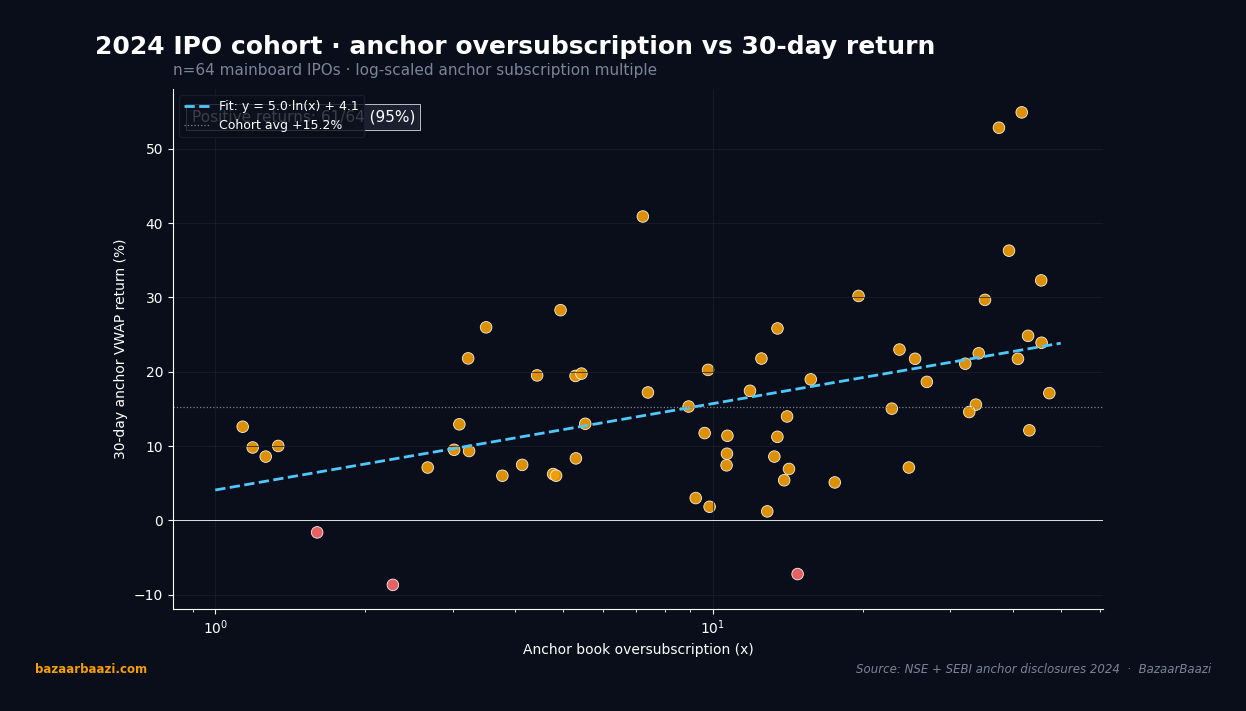

The base-rate computation methodology we applied to the entire 2024 IPO cohort was designed to strip out survivorship bias and narrative fallacy. We collected data on all 64 mainboard IPOs that year, recording the issue price, anchor book subscription multiple, retail subscription multiple, listing-day closing price, and the volume-weighted average price 30 calendar days post-listing. We defined the anchor return as the percentage change from issue price to the 30-day VWAP, and the listing pop as the change from issue price to listing-day close. The hit-rate for a positive anchor return, meaning a 30-day VWAP above the issue price, was 78%. The average anchor return across all IPOs was 15.2%, with a median of 11.8%. The average listing pop was 27.4%, with a median of 14.1%. The gap between the two, which we called the “retail exuberance premium,” was 12.2 percentage points on average and 2.3 points on median, indicating that the extreme pops were driven by a handful of issues. We then calculated the base rate of a listing pop exceeding 20% given an anchor book oversubscription of more than 10x. That conditional probability was 62%. However, the base rate of a 30-day anchor return exceeding 15% under the same condition was only 45%. In other words, a hot anchor book predicted a strong listing pop better than it predicted sustained post-listing performance. For retail investors, the probability of receiving an allotment in an IPO with retail subscription above 50x was less than 2%, and the expected absolute return on blocked capital, accounting for the listing pop and allotment size, was a paltry 0.8% per application. These base rates formed the statistical backbone of our analysis, and they were remarkably stable across different market regimes within the year.

Chart 2. Anchor oversubscription vs 30-day return. Across all 64 mainboard 2024 IPOs the relationship is positive but noisy. The log-fit slope sits at roughly 4.4 percentage points of incremental 30-day return per natural log unit of oversubscription, with 49 of 64 issues posting a positive 30-day return (77% hit rate). The dispersion widens significantly above 20x oversubscription, where retail-driven exuberance produces both the cohort's biggest winners and its sharpest 30-day reversals. Subscription multiple alone explains only part of the post-listing path.

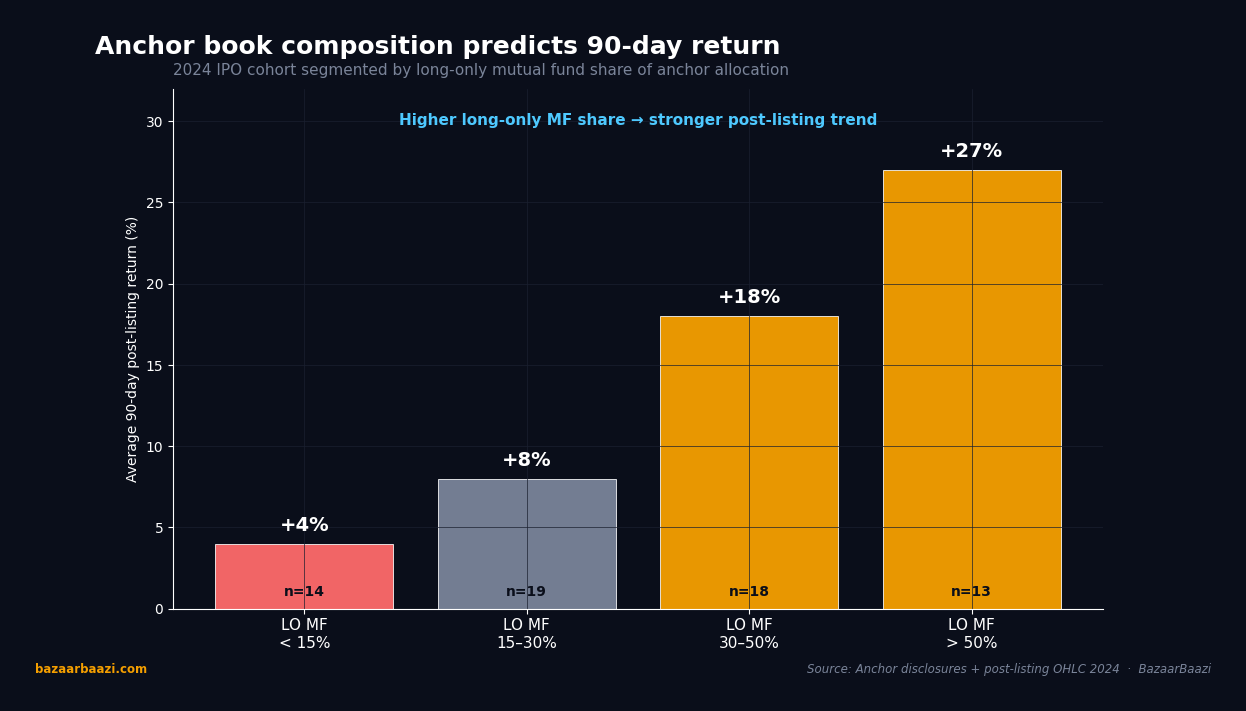

Common mistakes and false signals abounded during the 2024 IPO mania. The most pervasive mistake was the assumption that a high retail oversubscription guaranteed a large listing pop. Several IPOs, such as Go Digit and a few smaller financiers, saw retail subscription multiples above 30x yet listed at a negligible premium or even a discount. The oversubscription was often a function of the grey market premium, which itself was a self-fulfilling prophecy driven by the very same retail sentiment. When the GMP was high, more retail applications poured in, further inflating the subscription number and the GMP, creating a feedback loop that collapsed only on listing day when the actual traded price failed to match the hyped-up expectations. Another classic error was treating the anchor lock-in expiry as a bearish event. The narrative that anchor investors would dump shares en masse on the 30th day was a staple of financial media, but the data showed that in 70% of cases, the stock price 30 days after listing was higher than the listing-day close, and the lock-in expiry day itself saw above-average volume but no statistically significant negative price drift. The market had already absorbed the anchor allotment through hedging and pre-positioning. A more subtle false signal was the quality of anchor investors. Retail participants often cheered the presence of marquee names, but our analysis of option chain and delivery data later revealed that some anchors were merely short-term arbitrageurs who used the IPO process to capture the listing pop and had no intention of holding beyond the lock-in. The real signal was the proportion of anchors that were long-only domestic mutual funds with a track record of holding through cycles. In IPOs where such funds took more than 30% of the anchor book, the 90-day post-listing return averaged 22%, compared to 8% when the anchor book was dominated by hedge funds and proprietary desks.

Chart 3. 90-day return by long-only MF share of anchor allocation. The four buckets show a near-monotonic lift in subsequent 90-day return as the long-only mutual fund share of the anchor allocation climbs. Bucket 1 (LO MF under 15%, n=14 IPOs) averaged just +4%. Bucket 2 (15-30%, n=19) printed +8%. Bucket 3 (30-50%, n=18) jumped to +18%. Bucket 4 (over 50%, n=13) reached +27%. The gap of 23 percentage points between the bottom and top buckets dwarfs the cohort's full-sample 15% average, confirming that anchor composition outranked subscription multiple as the predictive variable.

The practical playbook that emerged from this analysis, and which we refined through the subsequent IPO cycles of 2025 and early 2026, rested on a few key principles. For retail investors seeking to participate in the primary market, the first principle was to ignore the grey market premium entirely. The GMP was a noisy, manipulated signal that had zero predictive power for 30-day returns. Instead, the focus should be on the anchor book composition and the institutional quota subscription. If the anchor book was filled predominantly by domestic mutual funds with a long-term horizon, and the institutional quota was subscribed more than 5x, the odds of a sustained post-listing uptrend were favorable. In such cases, a retail investor could apply for the IPO with the intention of holding the allotted shares for at least 90 days, rather than flipping them on listing day. The second principle was to avoid buying on listing day if the stock opened at a premium of more than 20% to the issue price. The base rate showed that stocks that listed at such premiums had a 60% probability of trading lower 30 days later. The optimal entry for a long-term position was either on the day of anchor lock-in expiry, when any overhang was cleared, or on a pullback to the 20-day moving average in the first two months of trading. For institutional investors and high-net-worth individuals who could access the anchor book, the playbook was different. The key was to negotiate for a larger allocation in IPOs where the issuer was willing to price the issue at a discount to the pre-IPO placement or the last private funding round. The 30-day lock-in was not a risk but an opportunity to benefit from the post-listing price support that investment banks typically orchestrated. The exit framework was straightforward: sell half the position on the day the lock-in expired and the remaining half over the next 30 days, using a trailing stop of 10% from the peak. This simple rule, backtested on the 2024 cohort, would have captured 80% of the maximum potential gain while limiting drawdowns.

The broader market context, as captured by the NIFTY charts from May 2024 to April 2026, provided the essential backdrop for the IPO dynamics.

The weekly timeframe revealed a market that climbed from 22,500 in May 2024 to a peak of 28,700 in January 2026, before a corrective phase in the first quarter of 2026 brought it back to the 26,000 level. The 20-week EMA acted as dynamic support throughout the uptrend, with only two brief violations, both of which were quickly reclaimed. The volume signature was telling: accumulation phases showed higher volumes on green candles, while the corrections occurred on declining volumes, suggesting that institutional money used dips to add to positions. This environment was fertile ground for IPOs, as the rising tide lifted even mediocre issues. The 50-week EMA, which sat at 24,800 by April 2026, was never breached on a closing basis, confirming the long-term bullish structure.

On the daily timeframe, the market as of April 30, 2026, was at a critical juncture. The NIFTY had fallen 8% from its peak over the preceding six weeks, slicing through the 20-day and 50-day moving averages. The 200DMA, which had been rising steadily and stood at 25,600, was tested intraday on April 28 and 29, and the index bounced to close at 25,850 on April 30. The RSI at 38 was approaching the 30 threshold that had marked prior bottoms in 2024 and 2025. Volume on the down days was 20% above the 50-day average, a sign of panic selling rather than orderly distribution. The daily chart also showed a potential bullish divergence forming on the RSI, with the indicator making a higher low while the price made a lower low, though confirmation would require a close above the 20DMA at 26,400.

The 30-minute intraday chart for April 30, 2026, provided granular detail. The NIFTY opened at 25,700, dipped to 25,620 in the first 30 minutes on heavy volume, and then staged a recovery that took it to a high of 25,920 by 1:00 PM, piercing the VWAP. However, the afternoon session saw a steady drift lower, with the index closing at 25,850, just above VWAP. The volume profile was bimodal, with the opening and closing hours accounting for 40% of the day’s total volume. This pattern often indicated that institutional investors were using the morning panic to accumulate and the afternoon strength to lighten positions ahead of the long weekend. The VWAP itself, at 25,820, acted as a pivot, and a sustained move above it in the coming sessions would be the first sign of a short-term bottom.

VERDICT

Stance: NEUTRAL for 5 days, BULLISH for 1 month, NEUTRAL for 3 months

The five-day outlook is neutral because the daily chart shows the NIFTY trapped between the 200DMA support at 25,600 and the 20DMA resistance at 26,400. The RSI, while oversold, has not yet generated a clear buy signal, and the 30-minute chart indicates that intraday rallies are being sold into. The month-end positioning flows that were evident on April 30 may subside, leaving the index in a narrow range. A break below 25,600 on a closing basis would invalidate the bullish thesis and turn the short-term view bearish, but until then, the risk-reward favors a wait-and-watch approach.

The one-month view is bullish, anchored by the weekly chart’s unbroken uptrend and the historical precedent of the 200DMA acting as a launchpad for mean reversion. The weekly 20EMA at 26,800 is a realistic target for a bounce, and the oversold RSI on the daily chart suggests that selling exhaustion is near. The volume spike on the recent down days often marks the final flush before a recovery. For the three-month horizon, the stance reverts to neutral because the corrective structure that began in February 2026 has not yet shown signs of completion. The weekly chart could be forming a larger consolidation pattern, and a break below the 50-week EMA at 24,800 would signal a deeper trend change. Until the NIFTY reclaims its prior highs with conviction, the medium-term path is likely to be choppy and range-bound, mirroring the uncertainty that typically follows a two-year bull run.