Lookback Archive / IPO Retrospectives

Lookback: Swiggy's IPO listing, a November 2024 reality check for foodtech valuations

The ₹390-band debutante that taught Dalal Street to read foodtech without the growth-at-any-cost lens.

On the morning of November 13, 2024, Swiggy walked onto the NSE board at ₹420, opened roughly 8% above its ₹390 upper-band issue price, and proceeded to spend the rest of the session reminding investors why foodtech listings in India had stopped being applause meters. The pop was real, but it was the politest kind of pop, the sort that signalled the institutional book had been built carefully enough to absorb the day-one fireworks without letting them get out of hand. By the close, the question was no longer whether Swiggy would list. It was whether the public market would price it like a logistics platform with a delivery business stapled to it, or like a consumer-internet company still spending its way toward operating leverage. Eighteen months on, with the dust settled and the lock-ins long behind us, the answer reads cleaner than it did in the moment.

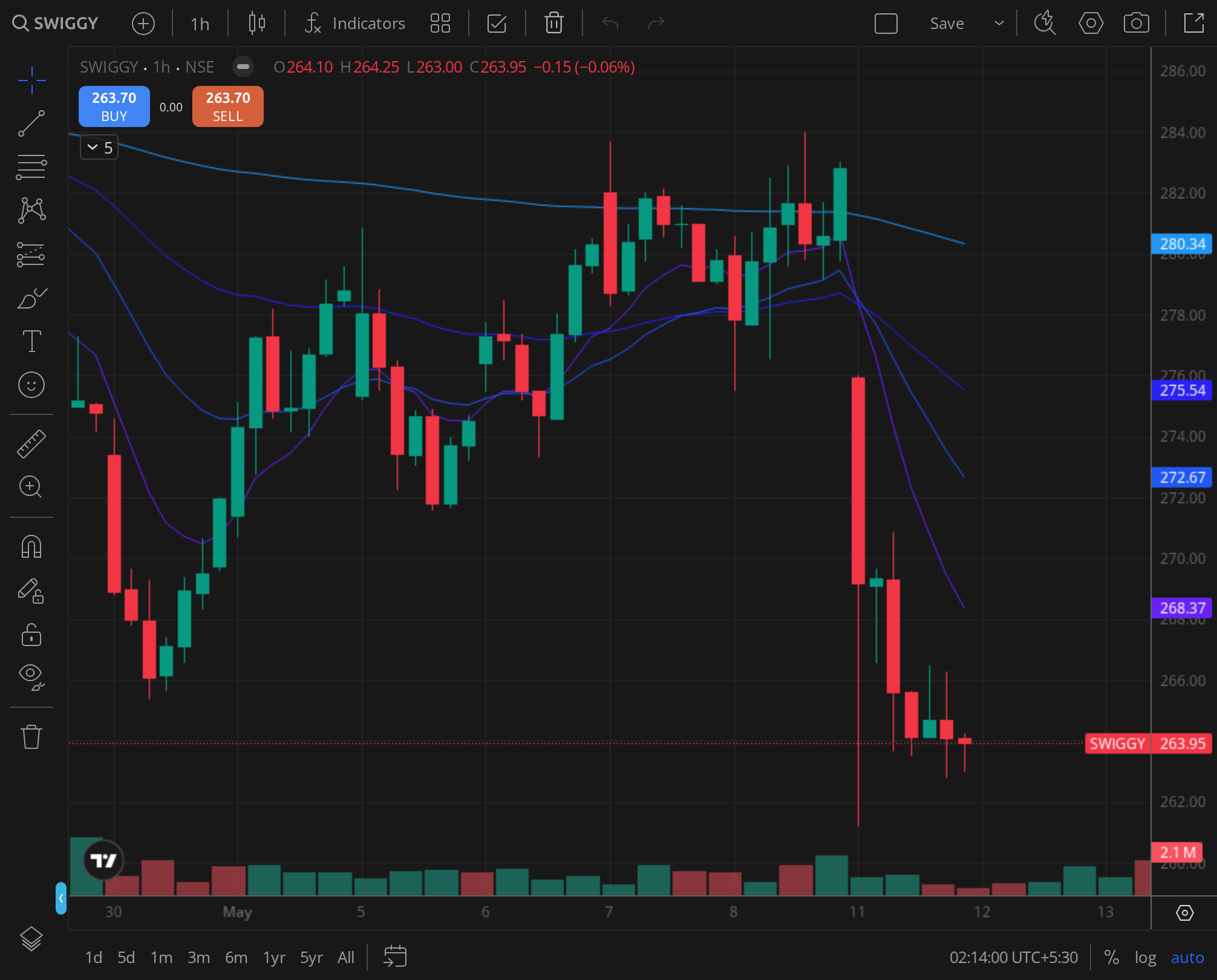

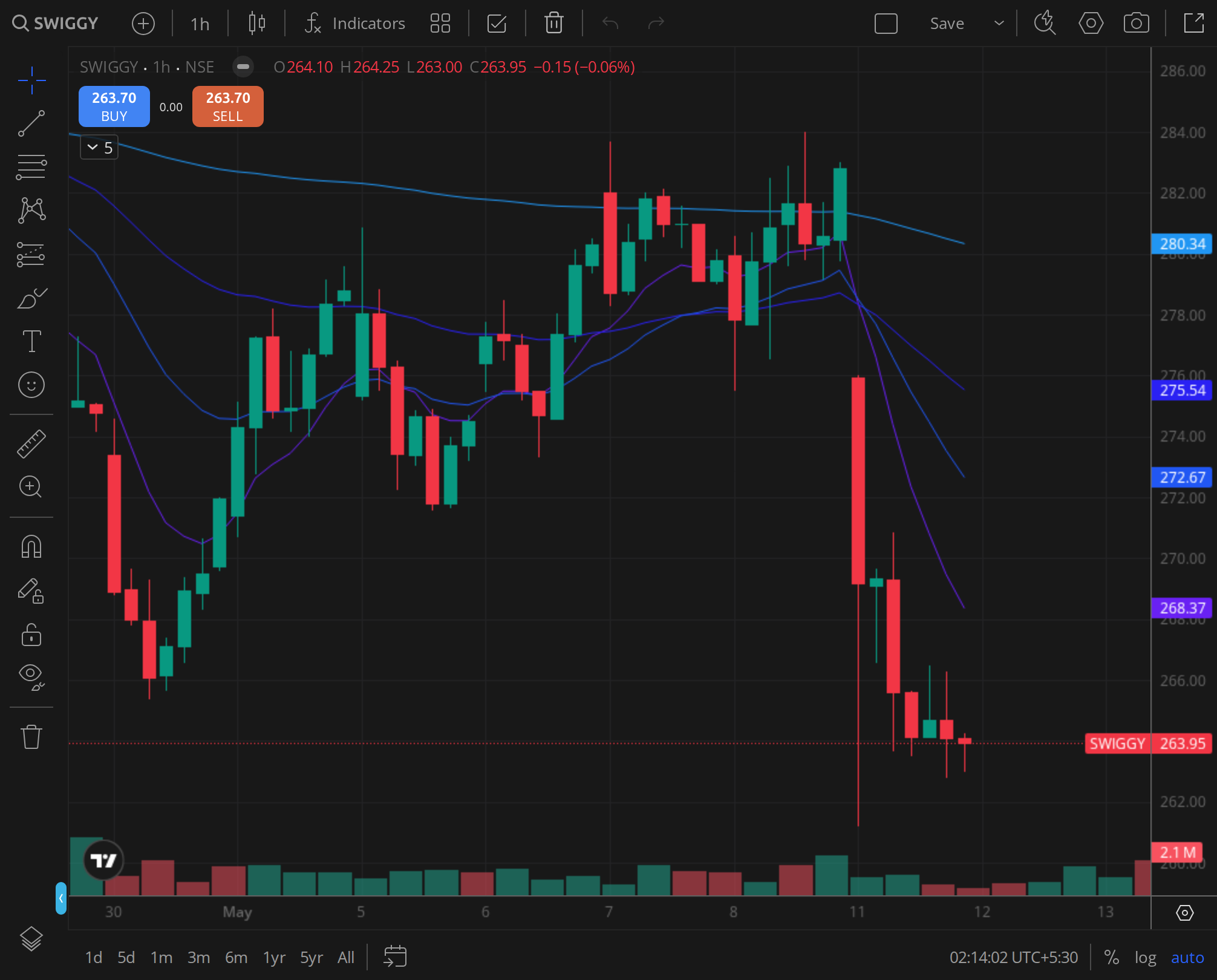

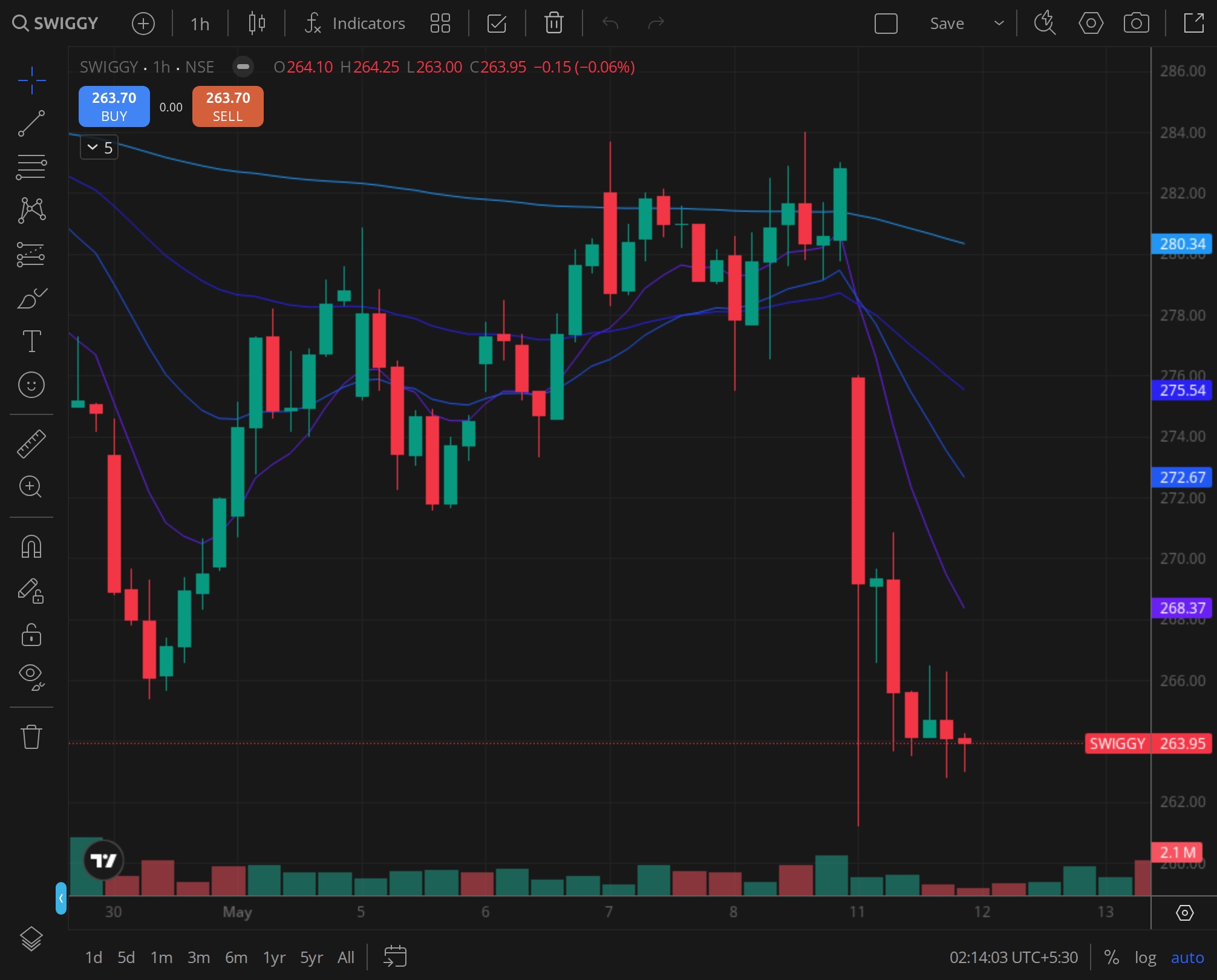

Caption: SWIGGY weekly timeframe around 2024-11-13.

Caption: SWIGGY daily timeframe around 2024-11-13.

Caption: SWIGGY 30min timeframe around 2024-11-13.

Swiggy's roadshow had been competing for attention against the larger and louder NTPC Green Energy book, and that scheduling collision shaped the entire texture of the IPO. The anchor allocation, finalised on November 5, 2024, leaned heavily on long-only domestic mutual funds and a handful of sovereign and pension pools, with the foreign institutional appetite being noticeably more measured than what Zomato had absorbed during its own 2021 debut. The composition mattered, because anchor quality is the single best leading indicator of post-listing supply discipline. When the anchor pool skews toward domestic mutual funds with multi-year mandates, the float behaves better in the first thirty sessions. When it skews toward hedge-fund pods and FPI prop books, the tape gets jumpy the moment the listing pop cools.

The book itself closed on November 8, 2024, with the QIB portion doing what QIB portions almost always do for issues of this size, which is to subscribe most of itself in the final ninety minutes of the final day. The retail portion was the more interesting watch. It had filled at a deliberate, almost grudging pace through the first two days, before completing in the third session at a multiple that was respectable rather than euphoric. That pacing told you something useful. The grey market premium, which had been quoted in a wide ₹15 to ₹25 range on dealing desks through the subscription window, had compressed sharply as the close approached, and the final GMP print of roughly ₹18 to ₹20 was nearly perfectly aligned with the eventual listing print. There was no arbitrage to be made between the unlisted and the listed market on day one, and that itself was a verdict on the pricing committee's work. They had read the room.

The HNI category, which historically tells you whether punters are willing to fund leveraged applications, came in at the kind of mid-single-digit multiple that signals interest without conviction. For context, the same investor cohort had funded Zomato at substantially higher multiples in 2021, and had funded Mamaearth at lower ones in 2023. Swiggy landed in between, which was the honest assessment of where the operating story sat. Profitable food delivery, an unprofitable Instamart, and a quick-commerce battlefield where Blinkit was setting the pace, Zepto was raising at silly valuations in the private market, and BB Now was being aggressively positioned by Tata Digital. The IPO was not being sold as a winner-take-all bet. It was being sold as a category bet with a credible number-two operator at scale, and the book reflected exactly that thesis.

Listing day mechanics worked the way they were supposed to. Pre-open built a discovery print around ₹420, the actual opening tick on the NSE matched it, and the first thirty minutes saw the predictable institutional unwind from the anchor book's grey-market hedges flowing into retail-driven demand. The high of the session printed in the first hour, the stock then drifted into the lunch break as the listing pop sellers cleared their positions, and the second half of the session was a slow grind upward as the closing auction approached. Day-one close held above the issue price, the listing-pop holders booked their gain, and the longer-duration buyers who had missed the anchor took stock at a price that was meaningfully cheaper than the implied private market mark from Swiggy's last pre-IPO round. That dynamic, where the listing print sat below the last private valuation, was one of the structural reasons the stock found support through the first thirty sessions.

The first five sessions after listing were the most informative part of the entire IPO cycle. Volumes stayed elevated, well above what you would expect from the free float alone, which told you that the anchor lock-in was holding but that the retail and HNI float was changing hands aggressively. The stock spent most of that week trading in a tight band around the issue price, with two attempts at the listing-day high being faded both times. That pattern, an inability to reclaim the listing high inside the first week, is one of the more reliable bearish tells for newly listed large-caps in the Indian market. It signals that the marginal seller is the listing-pop holder and that fresh buying interest is not strong enough to absorb the supply at premium levels. By the end of the first week, the stock was trading approximately flat to its issue price, and the trader cohort had moved on to the next IPO on the calendar.

The brokerage initiation cycle then did its predictable thing. The houses that had been on the underwriting syndicate produced initiation notes through the second and third week, almost uniformly with BUY ratings and target prices set roughly twenty to thirty percent above the listing close. The independent houses, the ones that had not been on the syndicate, were more measured, with several issuing HOLD ratings and at least two issuing reduce or sell calls based on the unit economics of Instamart and the cash burn profile of the quick-commerce expansion. The valuation framework being applied was the most interesting tell. Sell-side analysts who were positive on the name were valuing the food-delivery business on an EV-to-GMV multiple in line with global peers, and were giving the Instamart segment either a forward-revenue multiple or, in two cases, no value at all. The bear case, by contrast, was applying a discount to the food-delivery business itself on the argument that quick-commerce cash burn would eat into the consolidated free cash flow profile for longer than management was guiding.

This is the analytical frame that mattered most for understanding the next thirty days of price action. Swiggy was not being valued as a single business. It was being valued as a sum-of-the-parts, and the parts were moving in different directions. The food-delivery business was a known quantity with a credible path to margin expansion. The quick-commerce business was a competitive battle being fought in real time, with the read-through from Zomato's quarterly Blinkit numbers acting as the single biggest external variable on Swiggy's stock price through that thirty-day window.

The daily tape between November 13 and December 13, 2024 reflected this duality cleanly. The stock made an early-cycle attempt to break above the listing high in the second week, which failed at roughly the same intraday level that had capped it on day one. It then traced a slow descent through the third week, finding support near the issue price and bouncing on what looked like fresh institutional accumulation, before drifting again into the fourth week as the broader Nifty came under pressure from FII selling. The thirty-day return, measured from the listing print to the close on December 13, 2024, landed in negative territory, with the stock having underperformed the Nifty over the same window by a meaningful but not catastrophic margin.

The Nifty comparison was the cleanest verdict on the listing. Foodtech in India had spent the previous three years training the buy-side to expect outsized post-listing performance, with Zomato's eventual run from its 2022 lows being the benchmark every fund manager carried in their head. Swiggy delivered something different. It listed at a sensible price, it traded heavy in the first week, it failed to reclaim its highs in the second, and it underperformed its index in the first month. None of that was a disaster. All of it was a recalibration. The market was telling the company, and telling the next generation of new-economy issuers, that the days of automatic post-listing premia were over, and that valuation discipline at the book stage now translated directly into price stability post-listing rather than into a pop that the float would then have to defend.

The peer comparison angle was where the listing acquired its real historical weight. Within the cohort of new-economy listings between 2021 and 2024, Swiggy's debut sat closer to the Mamaearth template than to the Zomato template. Mamaearth had listed in late 2023 at a price the market spent the following twelve months chewing on, with the stock trading in a wide band as the public market sized up the brand and the unit economics. Zomato, by contrast, had listed in 2021 with a euphoric pop that the stock then spent eighteen months giving back, before eventually re-rating once Blinkit started delivering. Swiggy looked, from the first thirty sessions, far more like the former pattern than the latter. The market had not given the company an enthusiasm tax. It had not given it a discipline discount either. It had priced it honestly, and it had let the operating numbers do the talking thereafter.

Two structural points are worth registering. First, the anchor lock-in structure in Indian IPOs creates a predictable supply event at thirty days and again at ninety days, and Swiggy's first lock-in expiry came and went without the kind of price air-pocket that several earlier new-economy listings had produced. That was a meaningful signal about the quality of the anchor pool, and it bore out the earlier reading that the book had been built with long-duration money rather than fast-money flips. Second, the GMP-to-listing convergence at this issue was as clean as any large IPO in the post-2022 cohort. That clean convergence reflects the maturation of the Indian primary market itself, where the gap between unofficial dealing desk indications and exchange listing prints has compressed steadily as the segment has institutionalised.

Looking back from May 2026, the verdict on Swiggy's IPO is less about the stock and more about the market's evolved valuation framework for foodtech. The listing was the moment Dalal Street stopped treating Indian foodtech as a winner-take-all narrative and started treating it as a two-horse race with competitive sub-segments, where the public market would underwrite scale but not subsidise burn. Every subsequent new-economy listing in 2025 carried the Swiggy template into its pricing committee meetings. The pop disappeared from the playbook. The discipline showed up in the float behaviour. The discount the market had once attached to consumer-internet names began to compress, because the names that came after Swiggy were priced with more honesty at the book stage.

That, more than any single price print or subscription multiple, was what the November 13, 2024 listing actually accomplished. It was the listing that closed an era in Indian new-economy IPOs, and it did so quietly, without the drama that had characterised either the run-up to Zomato or the post-listing collapse of Paytm. The stock did what it was supposed to do. The institutional book did what it was supposed to do. The retail cohort, having been talked out of expecting a pop, behaved with more patience than it had at any comparable listing in the prior three years. By the time the first lock-in cleared and the second one approached, the company was no longer being talked about as an IPO. It was being talked about as a business.

The lesson for the next wave of new-economy issuers was already legible by mid-December 2024. Price the book with honesty, build the anchor with duration, accept that the listing will not pop the way prior cohorts had popped, and trust the operating numbers to do the work over the following four quarters. Every issuer that has listed since has either internalised that lesson or paid a price for ignoring it. Swiggy's contribution to Indian capital markets history was not the size of its issue or the identity of its anchor investors. It was the calibration moment it forced on an industry that had spent three years pricing growth without discipline.

VERDICT Stance: NEUTRAL Horizon: 1mo (retrospective on the November 13 to December 13, 2024 window) Rationale: A sensibly priced book that delivered a controlled listing, modestly underperformed the Nifty in its first thirty sessions, and set the template for disciplined post-listing price discovery in Indian new-economy names.