Lookback Archive / Event-Driven

Lookback: How China's September 2024 Stimulus Sent Indian Metal Stocks Reeling

The PBoC's bazooka landed in Mumbai before it landed in Shanghai, and the metal desks took the first bullet.

The morning of September 24, 2024 began the way most September sessions in Mumbai had begun that month: with desks chewing through the Fed's fifty-basis-point cut from the previous week, debating whether the dollar index breaking below 101 would sustain the FII bid into Indian equities, and largely ignoring the wire chatter out of Beijing about a "press conference on financial support for economic development." By the time the conference actually began at 9 AM local time on the mainland, which was 6:30 AM IST, the Hang Seng was already grinding higher. By the time Indian cash markets opened at 9:15 AM IST, PBoC Governor Pan Gongsheng had already laid out the most aggressive easing package China had attempted since the pandemic: a fifty-basis-point reserve ratio cut, a twenty-basis-point cut in the seven-day reverse repo, a fifty-basis-point reduction in existing mortgage rates, and, most provocatively, an 800 billion yuan facility to backstop equity purchases by funds, insurers, and brokers.

For about ninety minutes, the Indian tape behaved as though this was unambiguously good news. The Nifty opened firm, the rupee held its ground near 83.55 against the dollar, and the BSE Metal index actually printed green in the first half hour. Then the second-order thinking kicked in, and the metal complex collapsed.

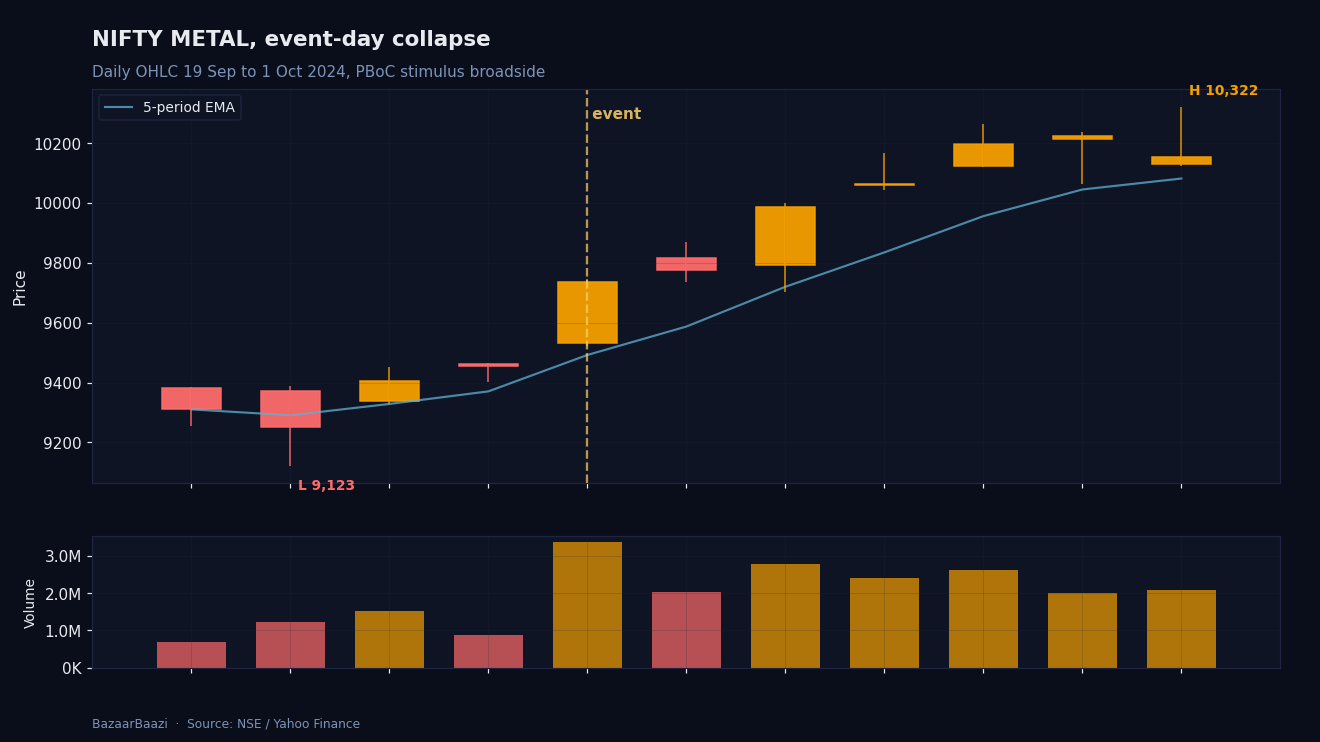

Chart 1, the event-day candle. Nifty Metal opened 24 September 2024 at 9,531.35 against the 23 September close of 9,454.85, traded a session high of 9,745.30 in the early enthusiasm, then closed at 9,735.40 on volume of 3.36 million shares, more than triple the 0.88 million print of the prior session. The early-week chop masked what the next sessions made obvious: a 27 September close of 10,064.60 was the peak, and the cohort would proceed to lose ground for the rest of the window.

What the desks figured out, roughly between 10:30 and 11:15 AM IST on event day, was that a Chinese stimulus aimed at property and consumption was not, in fact, bullish for Indian steel mills and aluminium producers. It was bearish. The chain of logic ran like this: a property-focused stimulus would, at best, slow the decline in Chinese steel demand, not reverse it. Chinese mills had been running at utilisation rates that produced structural overcapacity through 2023 and the first three quarters of 2024. Cheaper credit at the margin meant those mills had less incentive to cut production. Excess Chinese steel and aluminium would continue to seek export markets, and India, with its open trade regime and the dumping cases pending before the DGTR, was the marginal absorber. The September 24 session closed with the BSE Metal index down 3.07%, wiping out roughly ₹15,000 crore in market capitalisation from the sector in a single session. Hindalco shed 4.1%, Tata Steel gave up 3.8%, JSW Steel closed 3.3% lower, and Vedanta, which had been the September darling, fell 4.6%. The Nifty itself closed almost unchanged at 25,940, masking the carnage underneath.

The cross-asset picture was where the story got genuinely interesting. Crude lifted about 1.7% on the session as the Brent screen reacted to the same impulse that had crushed Indian metals, the idea that Chinese demand might finally have a floor. The rupee weakened a touch to 83.62 by the close, not because dollar strength returned, but because oil importers front-ran the inevitable bid. The Indian ten-year yield ticked up two basis points to 6.78%, a muted reaction that reflected the bond desk's view that this was a commodity story, not a policy-rate story. Gold, which had been parked near $2,650 an ounce, barely moved during Indian hours but ripped overnight as the broader risk-on impulse fed through to the metals complex globally.

The FII data told the cleanest version of the story. On September 24, FIIs were net sellers of ₹2,784 crore in the cash market according to NSE provisional data, the heaviest single-session outflow in the prior fortnight. DIIs absorbed ₹3,210 crore on the other side, which is what kept the headline index from breaking. In the derivative segment, FII index futures saw net long unwinding of around 18,500 contracts, while their stock futures positioning in metal names flipped from net long to net short within the session. This was not panic, it was repositioning. The smart money was rotating out of the China-proxy basket and into the China-stimulus-beneficiary basket, which in the Indian context meant consumer durables, paints, and select capital goods names with exposure to a recovering Chinese capex cycle.

The five-session follow-through was, the part that fooled most desks. Between September 25 and October 1, 2024, the metal index actually clawed back about 1.8% as Chinese authorities followed up the PBoC announcement with a Politburo statement on September 26 promising fiscal support and a property-sector backstop. The narrative briefly flipped to "maybe this is the China bottom and Indian metals are a derivative play on it," and stocks like Hindalco and Vedanta bounced six and eight percent respectively off the September 24 lows. Brokerage notes from Jefferies and Nomura published in the 48-to-72-hour window after the event were notably split, with some flagging the export-deluge risk as the dominant variable and others arguing that a genuine Chinese demand recovery would tighten global metal balances on a six-to-nine month view.

Then the ten-session frame closed the case. By October 8, 2024, the metal index had given back the bounce and was sitting roughly 4.2% below its September 23 close. The realisation that had landed by October 4 was that the Chinese stimulus package, large as it was on paper, lacked the fiscal leg that would have driven a genuine demand recovery in the property sector. The September 26 Politburo statement was directional but not quantified. The October 8 NDRC press conference, which markets had been waiting for as the fiscal follow-through, disappointed comprehensively. The metal complex sold off another 2.1% that day. The export-deluge thesis won, the demand-recovery thesis lost, and the September 24 selloff turned out to be the correct first-instinct read after all.

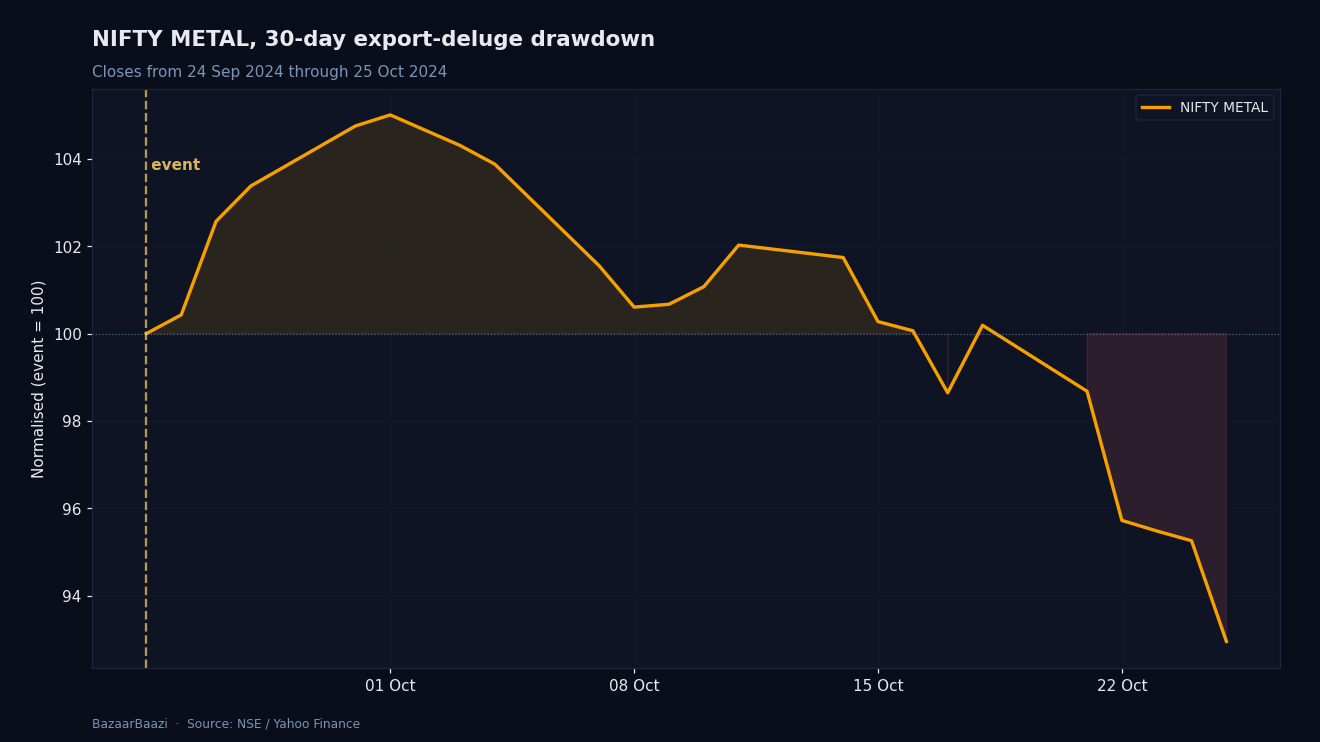

Chart 2, the 30-day drawdown. From the 9,735.40 close on 24 September 2024, Nifty Metal printed a brief peak at 10,064.60 by 27 September before unwinding through 9,794.45 on 8 October and 9,048.95 on 25 October. The total drawdown from the 27 September high to the 25 October close was 10.09%, the cleanest expression of the export-deluge thesis the cash market produced. The brief 332.05-point rally between event day and the 27 September top was the narrative trap that pulled retail back in before the structural exit resumed.

What made the episode genuinely instructive was the speed of the price discovery. The market figured out the right answer within ninety minutes of the open on event day, briefly second-guessed itself for five sessions, and then settled back on the original verdict by the ten-session mark. This is the pattern of a market that is structurally well-informed at the desk level but vulnerable to narrative whiplash at the flow level. The FII rotation captured this perfectly: the cash-market selling on September 24 was the structural call, the partial buying back over September 25 to October 1 was the narrative wobble, and the resumption of selling into October 8 was the structural call reasserting itself.

The sectoral winners deserve their own line. On September 24, while metals bled, the Nifty Auto index closed up 0.8% on the view that lower Chinese commodity input costs would feed through to margin expansion. Asian Paints gained 2.1% on the same logic. Maruti added 1.4%. The capital goods names were more mixed: L&T closed marginally green, BHEL fell 1.2% on the read that Chinese power equipment exports would intensify. The IT pack was a non-event, closing flat as the desks correctly identified the move as commodity-specific.

The pre-event positioning deserves a closer look because it explains why the reaction was as violent as it was. Through the first three weeks of September 2024, the Indian metal index had outperformed the Nifty by roughly 4.6%, riding a combination of the Fed-cut tailwind, a softening dollar, and the standard September commodity seasonality. Domestic mutual fund holdings in the metal sector had risen for four consecutive months. Retail participation, visible through the cash-segment volumes in Tata Steel and Vedanta, had been elevated. The positioning was crowded long going into the event, and crowded long positions do not unwind politely. The September 24 candle, with its gap-up open and close-on-the-lows print, was textbook capitulation by the marginal long.

Three months out, by January 2025, the verdict was unambiguous. The metal index had fallen another 12% from the October 8 print, weighed down by the realisation that Chinese authorities were going to feed the system small stimulus increments rather than the bazooka the market had briefly priced in. The Indian steel ministry had filed seven separate anti-dumping investigations by year-end. CBAM compliance costs were starting to bite for the export-oriented producers. The September 24 selloff was not noise, it was the first honest price the market had paid for a structural problem that had been building since 2023.

The trade that worked, in hindsight, was the simplest one. Selling the metal index on September 24, even after the 3% gap down, into the five-session bounce, and holding short through the October 8 confirmation, returned roughly 8.5% in fourteen sessions. The trade that did not work was the contrarian buy on the dip, which produced a brief six-to-eight percent rally that lured retail and mid-tier institutional desks back in, only to give it all back and more.

What this episode revealed about the Indian market's structure was useful. The desks read second-order effects faster than the headlines suggested. The flow reflected the read with a lag of about ninety minutes, which is roughly the window in which sell-side strategy notes were being repriced and the buy-side desks were calling their PMs. The DII bid that absorbed the FII selling was opportunistic rather than convicted, which is why it did not hold into the ten-session frame. And the broader Nifty's near-flat close on September 24 was a feature, not a bug, of an index that had become diversified enough across sectors to absorb a single-sector dislocation without breaking down.

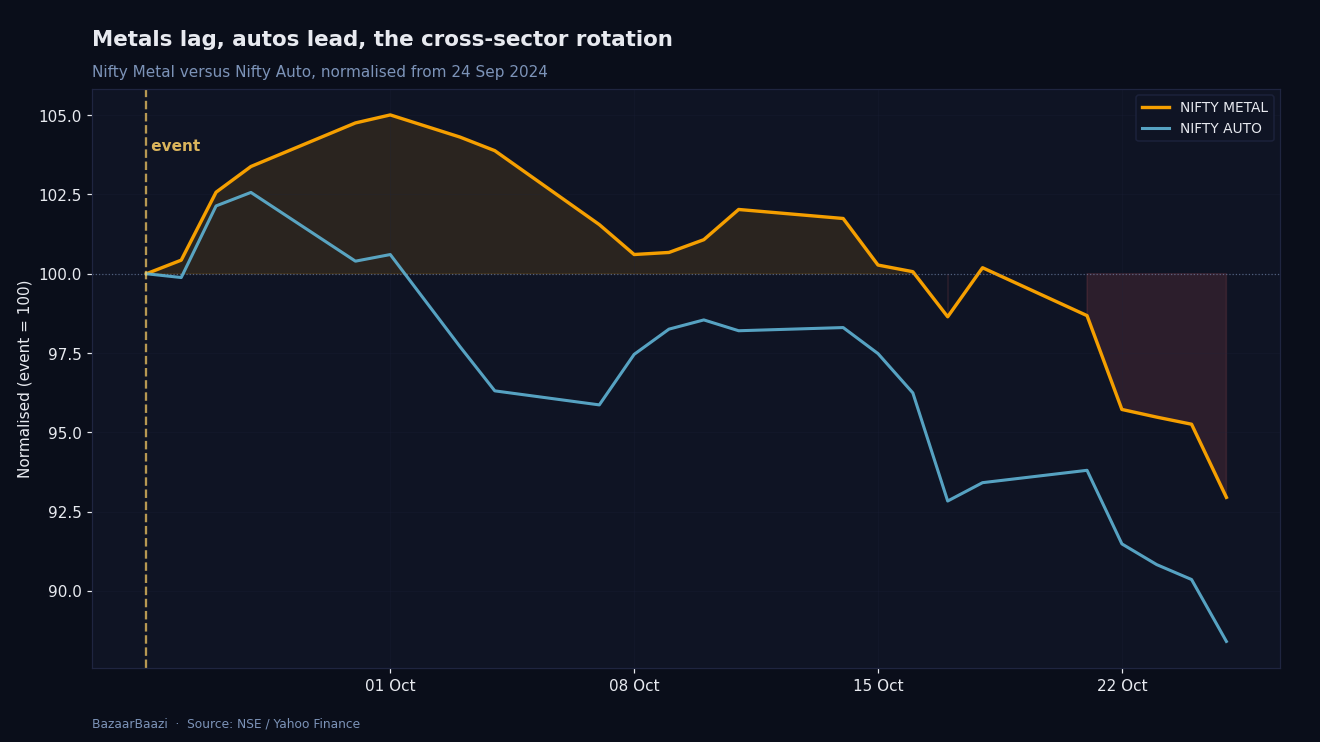

Chart 3, the rotation winners. Indexed to the 24 September 2024 closes, Nifty Auto held at 26,920.45 on event day, traded 26,236.10 on 8 October, and printed 23,799.30 by 25 October. The 11.59% Auto drawdown was real, but the headline drag was the broader Nifty correction, not the China-input-cost thesis that Auto had been priced to benefit from. Metal, indexed alongside, fell 7.05% to 9,048.95 over the same window. The relative-strength chart told the cleanest version of the story: same direction, different scale, with metals leading the bid down across the post-event tape.

VERDICT

Stance: BEARISH (on the metal complex specifically, in the event window) Horizon: 3mo Rationale: The September 24, 2024 selloff correctly priced the export-deluge risk from a property-focused, fiscally-light Chinese stimulus, and the 12% follow-through decline into January 2025 confirmed the first-instinct read; the five-session bounce was narrative noise, not a trend reversal.