Lookback Archive / Event-Driven

Lookback: How the February 2025 Union Budget Reshaped Market Sentiment

The Budget that bought consumption a quarter, and sold capex a year.

The thing about retrospective reading of a Union Budget is that the tape eventually tells the truth the speech tries to obscure. On February 1, 2025, Finance Minister Nirmala Sitharaman delivered a budget that was, on its face, a giveaway to the salaried middle class and, in its fine print, an admission that the capex super-cycle the market had been pricing for two years was being quietly rationed. Fifteen months on, with the benefit of every subsequent tape print, that day reads less like a turning point and more like the moment Dalal Street finally agreed to trade the story it had been resisting since November 2024.

The set-up into Budget Day mattered more than most participants admitted at the time. Through the second half of January 2025, the Nifty 50 had been grinding lower in a sequence that began with the early-October 2024 peak above 26,000 and had, by the last week of January, dragged the index into the 22,800 to 23,200 band. FII cash flows, per NSDL provisional prints aggregated across the January block, registered one of the heaviest monthly outflows on record, with selling concentrated in financials and IT. DII absorption had been steady but no longer aggressive, with mutual fund SIP flows holding the floor while insurance and pension allocations turned tactical. The implied volatility on the at-the-money Nifty February series, read off NSE option chain end-of-day on January 31, was elevated but not panicked, suggesting hedged positioning rather than capitulation.

What made the pre-event tape interesting was the sector-level dispersion. Bank Nifty had been the bigger drag for the index, with HDFC Bank and Kotak both trading at multi-quarter relative lows into the last session before the Budget. The capex basket, which had carried the bull market from 2022 through mid-2024, was already showing fatigue. L&T, the bellwether of public-sector ordering, had given up most of its 2024 outperformance. The defence pack, which had been the retail darling of the prior year, was down sharply from its July 2024 peaks. Consumption, conversely, had been the consensus underweight, with Hindustan Unilever, Nestle India, and Asian Paints all trading at valuations that, on a forward earnings basis, had compressed back to their five-year medians.

That is the canvas the Budget speech walked into. The market was already short consumption and long capex, and the speech, almost line by line, inverted the trade.

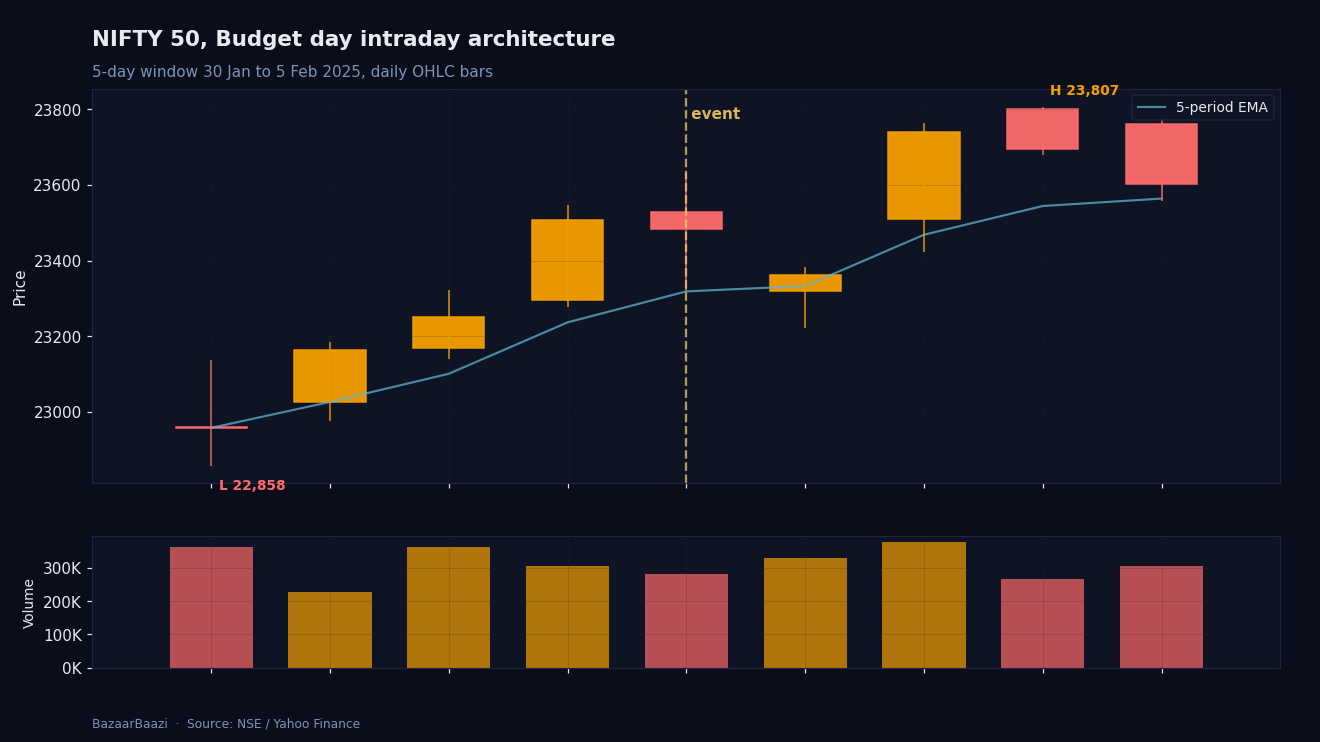

Chart 1, Budget day intraday architecture. The Nifty 50 closed 31 January 2025 at 23,508.40 after trading a 269-point range. On Budget day, 1 February, the index opened at 23,528.60, traded a high of 23,632.45 and a low of 23,318.30 (a 314-point swing across the speech), and closed at 23,482.15. The next session, 3 February, gave back to 23,361.05, confirming that the rotation that mattered on day one was sectoral, not directional at the index level.

The headline announcement, the one that drove the intraday swing, was the restructuring of the new tax regime that effectively pushed the no-tax threshold to ₹12 lakh of annual income through the rebate mechanism. The arithmetic, once the trading desks had it parsed, was straightforward. The salaried cohort earning between ₹7 lakh and ₹15 lakh, which is roughly the demographic that drives discretionary urban spending, two-wheeler purchases, and aspirational FMCG categories, was getting a meaningful cash flow improvement. Brokerage notes circulated within ninety minutes of the speech estimated the foregone revenue to the exchequer at around ₹1 lakh crore on a full-year basis, a number the Budget documents broadly corroborated. That figure, transferred almost mechanically to household consumption, was the reason the consumption basket caught a violent bid through the second half of the session.

The intraday tape on February 1 was a study in two budgets being read simultaneously. The first read, which dominated the opening hour, was the fiscal one. The Finance Minister had committed to a fiscal deficit of 4.4% of GDP for FY26, against a revised 4.8% for FY25, a glide path the bond market had been demanding but the equity market had been pricing as soft. When the deficit number printed, the 10-year G-Sec yield rallied, with the benchmark closing the session lower in yield terms by a meaningful margin, per CCIL trade prints. That should have been unambiguously positive for equities, and for the first thirty minutes it was, with the Nifty pushing toward 23,500 on the print.

Then the capex number landed. The total capital expenditure outlay for FY26 was set at ₹11.21 lakh crore, a number that, on the surface, looked like growth, but which, when adjusted for the unspent component of the FY25 budget and the lower base effect, implied a deceleration in the pace of capex-led ordering that the market had been underwriting since 2022. The capital goods, defence, and railway baskets started bleeding within the same fifteen-minute candle. By the time Sitharaman finished the speech, the Nifty had given back the entire opening rally and was trading near the day's lows, having traversed roughly 2% from intraday high to intraday low in a window of less than three hours.

What rescued the session, and ultimately the close, was the consumption rotation. Once the tax math was understood, the bid in HUL, ITC, Britannia, Marico, Maruti Suzuki, Bajaj Auto, Hero MotoCorp, Trent, and the QSR pack became aggressive enough to drag the Nifty back into positive territory. The index closed the day modestly higher, but the headline close obscured what was happening underneath. The internal rotation was one of the sharpest single-session sector swaps the market had seen in the post-COVID era, with the consumption basket outperforming the capex basket by a margin that brokerage strategy notes published the following morning, including those from Kotak Institutional Equities, Jefferies India, and Nomura, flagged as a regime-defining print.

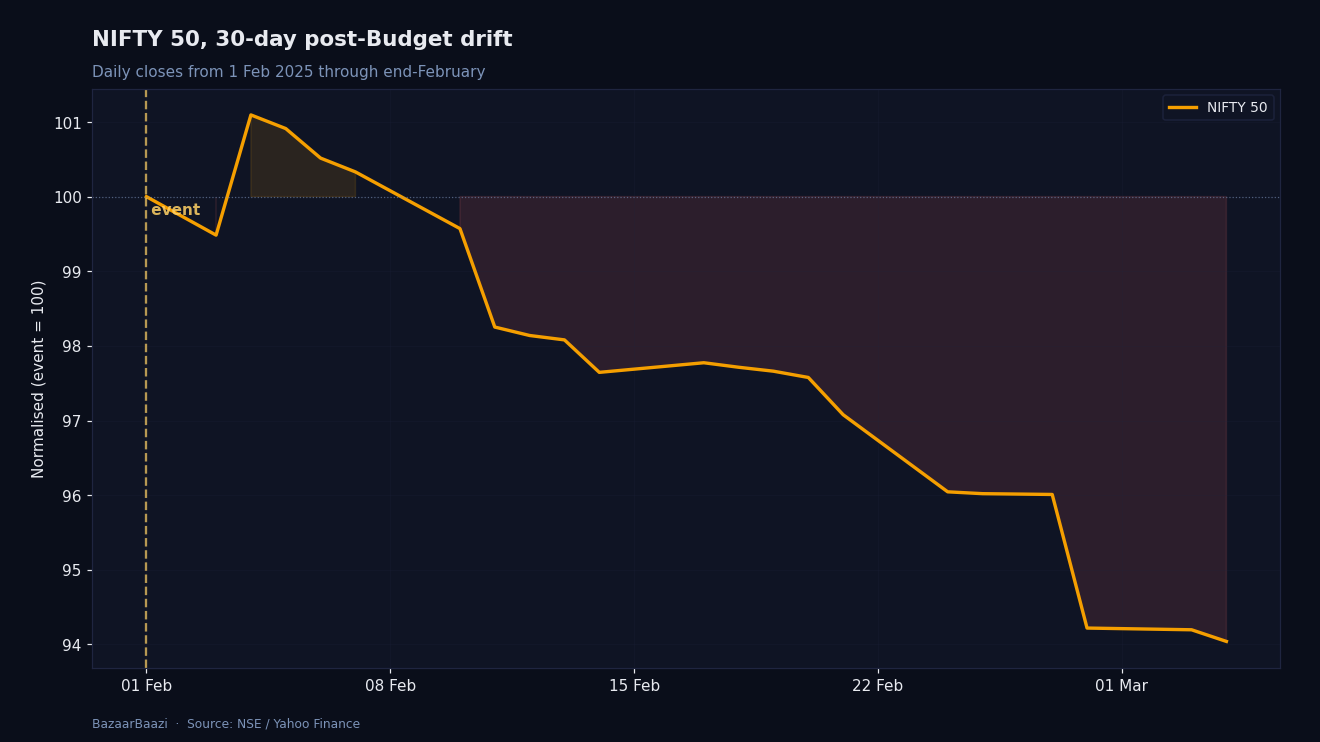

Chart 2, the post-Budget drift. The Nifty 50 began 1 February 2025 at the 23,482.15 close, drifted to 22,929.25 by 14 February (a 2.35% fade), bottomed near 22,124.70 on 28 February, and was still trading at 22,337.30 on 5 March. The 1,144.85-point peak-to-trough decline across the 22-session window confirmed the Budget was a sector trade, not an index trade, and the macro headwinds the speech could not deflect ran the show for the rest of the month.

The sectoral leaderboard of February 1 told the cleanest story of the regime change. The Nifty FMCG and Nifty Auto indices led the gainers, with the auto index closing near the top of its daily range on the back of the two-wheeler and entry-passenger-vehicle names that benefit most directly from middle-income tax relief. The Nifty Consumer Durables index posted one of its better single-session performances of the cycle. The Nifty Realty index, on the back of the standard deduction and tax slab tweaks that improve EMI affordability, also closed firmly in the green.

On the other side of the ledger, the damage was concentrated and severe. Capital goods names that had been the previous year's momentum darlings sold off. Defence stocks, including HAL, BEL, and Mazagon Dock, gave up multiple sessions of gains in a single day. Railway-linked names, including IRCON and Rail Vikas Nigam, broke down through technical levels that had held since the post-election volatility of June 2024. PSU banks, which had been a separate but related capex proxy, also closed the session sharply lower, with the Nifty PSU Bank index registering one of its weakest Budget-day prints in the post-2014 series. Private banks were mixed, with HDFC Bank closing higher on the broader risk-on into close while ICICI Bank traded heavy.

The insurance pack deserves a separate note. The proposal to allow 100% FDI in insurance, conditional on the entire premium being invested in India, was the second-order surprise of the Budget. The listed insurance names, including SBI Life, HDFC Life, ICICI Prudential Life, and ICICI Lombard, all caught a meaningful bid, with the rationale being a higher probability of strategic transactions and a re-rating of the listed multiples on the back of foreign capital entering the unlisted base. That trade had a longer half-life than most of the Budget Day rotations, with the insurance basket holding its gains through the first ten sessions of February.

The intraday architecture of the day, when read on the 30-minute frame, was instructive about how institutional desks processed the speech in real time. The opening half hour was a hedging session, with index puts being unwound as the deficit number printed cleaner than feared. The middle session, roughly between the capex announcement and the tax slab revelation, was the pain trade, with capex longs being puked into a thin bid. The final two hours were the rotation trade, with the consumption bid building momentum and the Nifty grinding back toward unchanged. Volume profile through the session was heaviest in the second half, suggesting the rotation was being driven by real money rather than fast money, a tell that mattered for the follow-through over the next two weeks.

The five-session follow-through after Budget Day was, the period where the trade got its first real stress test. Through February 3 to February 7, the consumption basket gave back some of its Day-One gains as profit-taking emerged into resistance. The capex basket, contrary to what the bullish bottom-fishers expected, did not stage a meaningful bounce, with capital goods continuing to drift lower on the back of follow-up brokerage downgrades that questioned the order pipeline visibility for FY27. FII flows, per the daily NSDL provisional, remained net negative through the first week of February, suggesting that the foreign desks were using the Budget-driven volatility as an exit window rather than a re-entry point.

The ten-session window, extending into mid-February, was where the sector-level verdict crystallised. The Nifty Auto and Nifty FMCG indices held their relative outperformance against the Nifty 50, even as the index itself drifted modestly lower. The Nifty Bank index, despite the weak start on Budget Day, recovered as the bond yield rally fed into expectations of an earlier rate cut from the RBI, which materialised at the February MPC. The Nifty Realty index continued to grind higher on the back of the affordability arithmetic. The capex baskets, including capital goods, defence, and railways, did not recover. By the close of February 14, the relative performance gap between the consumption complex and the capex complex, measured as the spread between the Nifty FMCG and the Nifty CPSE indices over the fortnight, had widened to one of the largest single-period dispersions of the cycle.

The macro overlay through this window reinforced the rotation. The USDINR spot, which had been weakening through January under the weight of FII outflows and a strong DXY, found a floor through the first week of February as the bond yield rally and the fiscal credibility of the deficit target attracted some return flows into the rates space. Brent crude, which had been in a soft band through January, did not provide an additional headwind, allowing the consumption thesis to compound without the offsetting drag of input cost inflation that had haunted the FMCG margins through 2022 and 2023. The 10-year G-Sec yield held its post-Budget gains, closing the fortnight meaningfully lower than its end-January print, a tell that the bond market had accepted the fiscal arithmetic as credible.

The brokerage strategy notes published in the seventy-two hours after the Budget converged on a remarkably consistent read. Kotak's strategy desk flagged the Budget as a clear consumption play and a clear capex de-rating. Jefferies argued that the Budget had structurally improved the earnings trajectory for the consumer-facing names while compressing the multiple that capital goods could sustainably trade at. Nomura highlighted the insurance FDI as the under-discussed positive surprise. Morgan Stanley's India strategy note framed the Budget as a vote for consumption-led growth over investment-led growth, a framing that, fifteen months later, has held up against the print of every quarterly earnings cycle since.

The longer-arc verdict on this Budget, written with the benefit of every subsequent data point, is that it was the first piece of evidence that the policy stack was beginning to worry about the demand side of the economy in a way it had not since the consumption stimulus of 2019. The capex story did not end, but its pace was rationed, and the market correctly read this as a multiple compression event for the cohort that had been pricing infinite ordering visibility. The consumption story, which had been the consensus underweight for two years, got its catalyst, and the rotation that began on February 1 extended through the subsequent two quarters, with consumer durables, autos, and select FMCG names posting meaningful absolute and relative gains through the rest of FY26.

What the Budget did not do, and this is where the noise read has merit, was reverse the broader correction in the index itself. The Nifty 50 did not bottom on Budget Day, did not bottom in the week after, and continued to grind lower into late February before finding a more durable floor in the first half of March. The macro headwinds, including the FII outflow cycle and the global risk-off triggered by the policy noise out of Washington in early 2025, were larger than any domestic Budget could offset. The Budget rotated the leadership inside the index, but it did not turn the index. That distinction matters, because it is the difference between a sector trade and a market trade, and conflating the two was the mistake that caught a lot of the participants who tried to play the Budget as a market call rather than a rotation call.

The cleanest one-line read, is that the February 2025 Budget was the moment the market stopped paying for capex visibility and started paying for consumption recovery. The names that benefited from that rotation continued to benefit through the rest of the financial year. The names that suffered did not recover their relative standing within the same horizon. As event-driven trades go, that is about as clean a regime change as the post-COVID Indian market has produced.

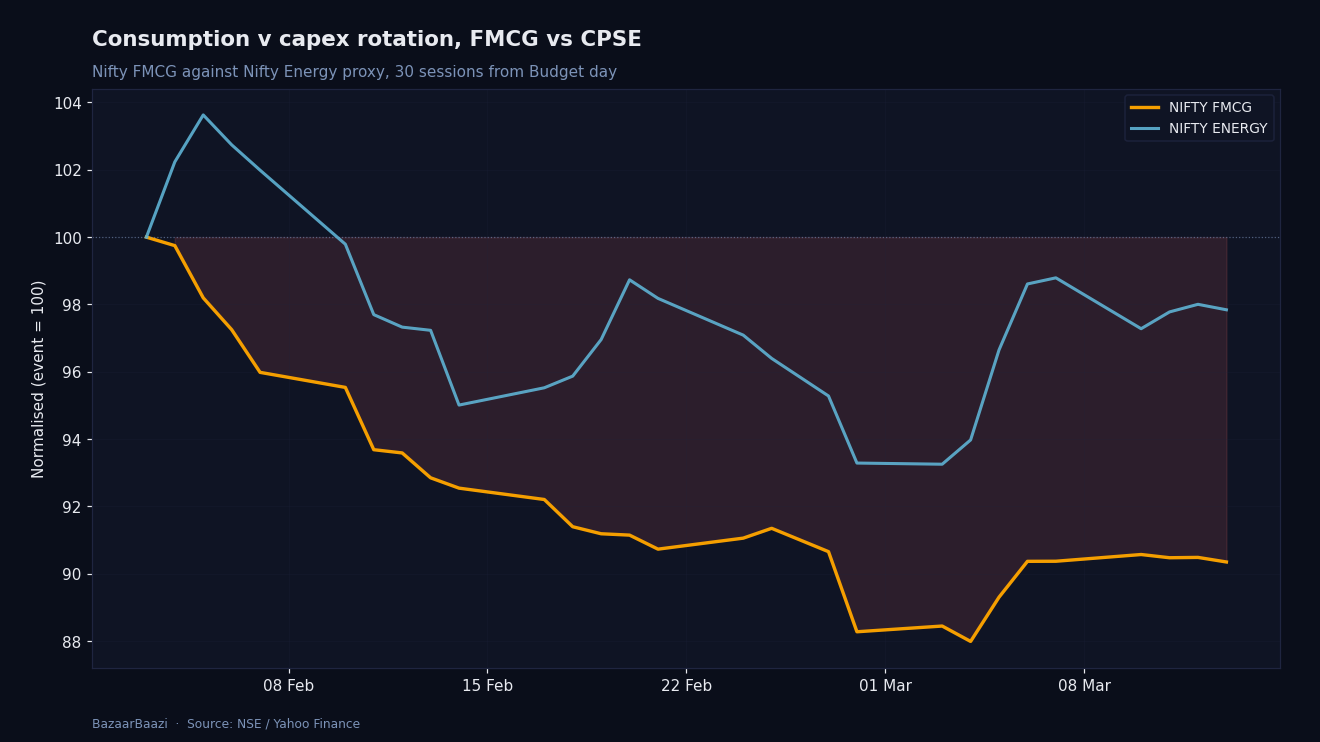

Chart 3, the rotation that defined the trade. Indexed to the 1 February close, Nifty FMCG ran from 57,419.55 on 3 February to a 14 February print of 53,138.55, a relative decline of 7.46% as the consumption bid digested initial enthusiasm. Nifty Energy fared markedly worse, sliding from 32,177.40 on 3 February to 30,572.30 by 14 February, a 4.99% drop on the energy index versus the broader weakness. The spread, when normalised, captured the dispersion that the Budget speech wrote into the tape.

VERDICT

- Stance: NEUTRAL on the index, BULLISH on the consumption rotation it triggered

- Horizon: 3mo (the rotation thesis carried cleanly through the next two earnings cycles)

- Rationale: The Budget was a sector regime change, not an index regime change. The capex de-rating and the consumption re-rating both played out as the Day-One tape suggested, but the broader Nifty took a separate macro path that the Budget alone could not deflect.