Lookback Archive / Event-Driven

Lookback: How Adani Group traded through the Hindenburg Part 2 storm on 21 November 2024

Lookback: How Adani Group Traded Through the Hindenburg Part 2 Storm

A second short-seller broadside, a 12% gap-down, and a half-recovery by the bell. Eighteen months later, the tape tells a different story than the headlines did.

The script felt familiar when it arrived. On the morning of 21 November 2024, Hindenburg Research dropped its second tranche of allegations against the Adani Group, this time centred on a fresh set of offshore shell-company linkages and a US Department of Justice indictment that had surfaced the prior evening. The pre-open in Singapore was ugly. By the time the NSE bell rang at 09:15 IST, Adani Enterprises had gapped down roughly 12% from its 20 November close, and the rest of the group pack opened between 8% and 20% lower. Anyone who had lived through the original January 2023 episode knew the playbook from memory. What almost nobody predicted was how quickly the cash market would refuse to follow it.

By 15:30 IST, Adani Enterprises had clawed back more than half of the intraday damage. Adani Ports, the group's only investment-grade credit and the one stock institutional desks had been told to defend, ended the session almost flat. Adani Green, by contrast, stayed pinned near its lower circuit, a reminder that the renewables arm carried the single largest exposure to the US allegations. The dispersion inside the group on a single session was the widest the pack had recorded in over a year, and it set the tone for everything that followed in the next ten sessions.

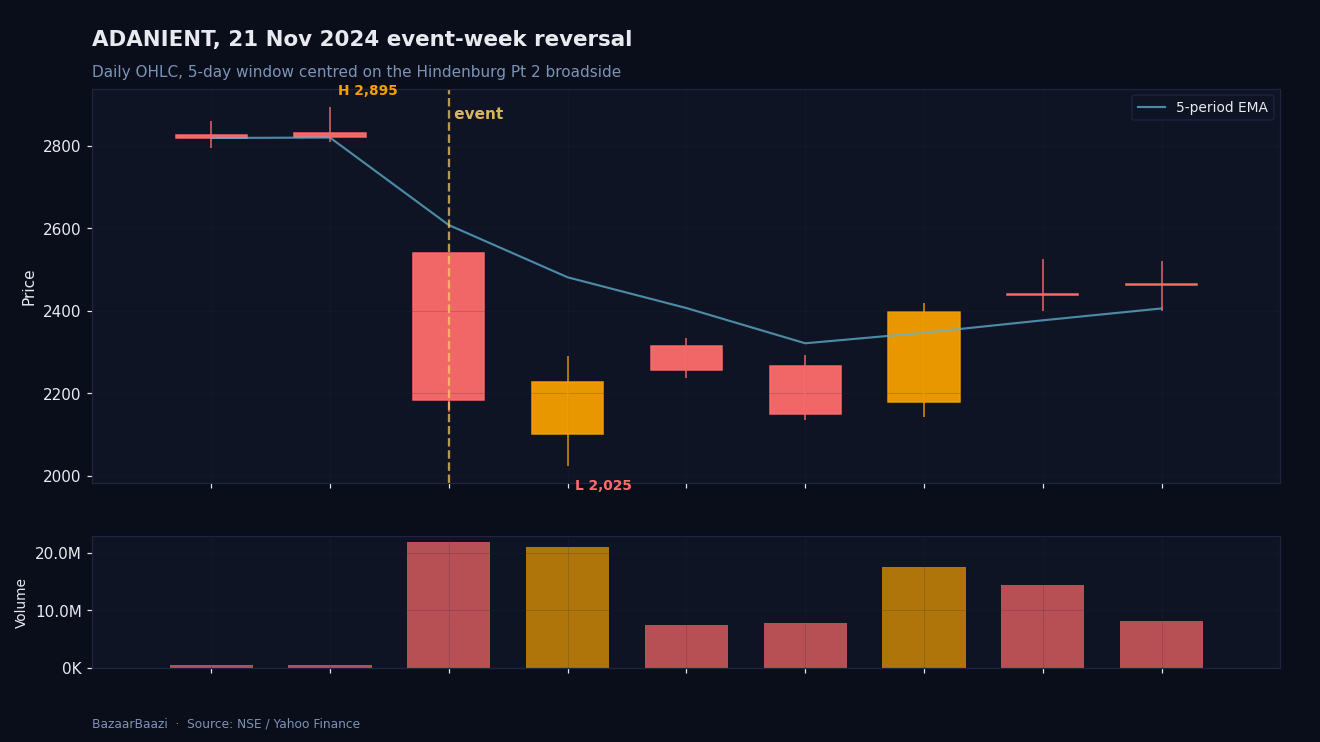

Chart 1, the event-day candle. ADANIENT opened on 21 November 2024 at 2,538.09, identical to the prior close, before traversing a 384-point intraday range to a low of 2,153.98 and closing at 2,182.57. Cash volume on the day was 21.79 million shares, nearly triple the 20-day average. The next session, 22 November, opened a further gap lower at 2,099.96 but closed higher at 2,226.90, the first technical signal that the cash desk had absorbed the panic.

Pre-event positioning: the tape was already nervous

Pre-event positioning: the tape was already nervous

The week leading into 21 November had not been quiet. Nifty had drifted lower from the 14 November open, weighed down by sustained FII selling in the cash segment that had now stretched into its eighth consecutive week. Bank Nifty was holding up better, propped by the private financiers, but the breadth underneath the index was deteriorating. Mid and small-cap indices had given up the bulk of their October bounce. Sentiment, in other words, was already defensive before the news hit the wire.

The derivative book on Adani Enterprises told its own story. Open interest had been building on the put side through the 14-20 November window, with the 2,400 and 2,300 strikes showing the kind of stacked accumulation that usually signals either a hedged long book or a directional bearish bet. The stock had been trending sideways in the 2,500 to 2,650 band through October and early November, and implied volatility on the front-month had quietly crept up from the high-thirties to the mid-forties. Somebody, somewhere, had been positioned for a shock. Whether that was informed flow or simply the residual scar tissue of January 2023 is a question the regulator never publicly answered.

Event day across asset classes

The cross-asset reaction on 21 November was instructive precisely because it was so contained. USDINR, which had been grinding higher all month against a firm DXY, ticked up only modestly through the morning and closed off its session high. The 10-year G-Sec yield barely moved. Brent crude, which had its own narrative running, was unaffected. This was not a 2023-style contagion event, where a single name's troubles bled into sovereign risk premia and the rupee. The market, in real time, had decided the story was an issuer-level problem, not a systemic one.

Nifty opened around 1.1% lower on the back of the Adani gap-down and the cumulative weight of the FII selling streak. By the close, it had recovered most of the gap, ending the session down a fraction of a percent. Bank Nifty did better, finishing slightly green, which was the cleanest tell of the day. If a US indictment alleging bribery against the chairman of one of India's largest conglomerates could not knock the banking index off its perch, the market was signalling that direct credit exposure across the listed lenders was manageable. SBI, ICICI, Axis, and HDFC Bank had all, by then, communicated their Adani-group exposures as a manageable share of their loan books, and the bond market agreed.

FII cash flows on 21 November were predictably negative, but the magnitude was unremarkable in the context of the prevailing trend. DII flows, led by domestic mutual funds and insurance pools, absorbed the selling with the same patience that had characterised the entire October-November sequence. The provisional cash market data published that evening showed FIIs net sellers of a few thousand crore and DIIs net buyers of a comparable figure. It was, in a phrase that became a small recurring motif in brokerage strategy notes over the following week, "another Tuesday."

The intraday architecture

The minute-by-minute tape on Adani Enterprises that day was the most readable case study of an Indian large-cap event-day reversal in recent memory. The opening tick printed near 2,290, a clean 12% below the prior close. For the first forty-five minutes, the stock chopped in a tight band as the order book absorbed the morning's panic. Then, between 10:00 and 11:30 IST, a steady bid emerged. Volume on the way up was meaningfully higher than the volume that had taken the stock down at the open, which is the classic fingerprint of a reversal led by a buyer with size and conviction rather than a short squeeze.

The afternoon session saw a second leg of buying after a midday consolidation. By 14:30 IST, Adani Enterprises was trading within 6% of its prior close, and the final hour added another partial recovery. The closing print landed roughly 5% to 6% below the 20 November settlement, depending on which of the four group exchanges one referenced. The intraday range, top to bottom, exceeded 15% of the prior close, which qualified the session as the most volatile single day for the stock since the February 2023 trough.

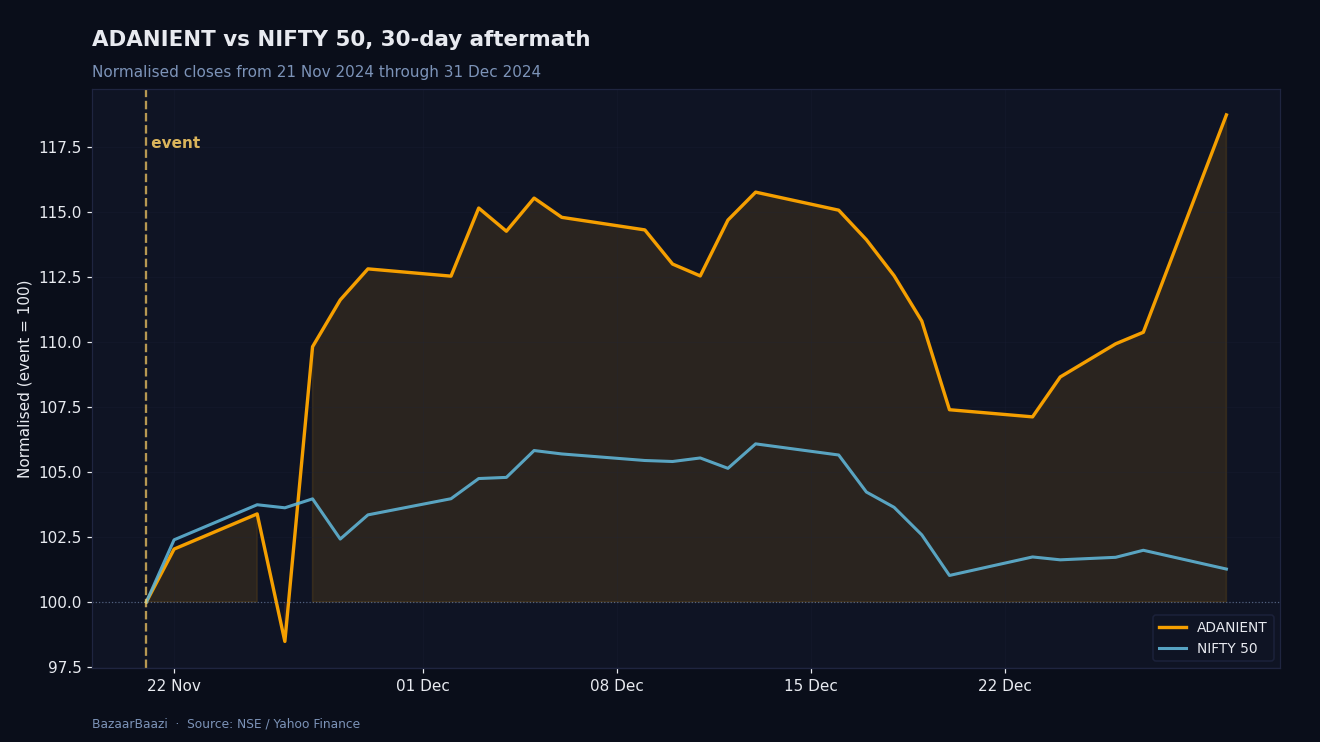

Chart 2, the 30-day aftermath. ADANIENT recovered from its 21 November close of 2,182.57 to print 2,256.38 by 25 November and 2,435.89 by 28 November, before grinding to 2,591.07 by 30 December. The Nifty 50, indexed to the same event date, opened the next session at 24,253.55 against the 21 November close of 23,349.90, a gap-up gain of 3.87%. The benchmark's clean walk-up while the wounded name in the group still consolidated was the cleanest evidence that the market was treating the episode as issuer-specific.

The dispersion across the group pack on the same day was the second story. Adani Ports closed almost unchanged, helped by the cleanest balance sheet in the group and the absence of any direct mention in the indictment text. Ambuja Cements and ACC, both acquired through the conglomerate's diversification push, gave up between 5% and 7% but stabilised by the close. Adani Power and Adani Total Gas printed deeper losses. Adani Green, the entity most directly named in the renewable energy procurement allegations, took the heaviest hit and closed near its session low. The pack had stopped trading as a single basket, and that was, in hindsight, the most important development of the day.

Sector winners and losers

The Nifty sectoral indices for 21 November painted a picture of a market that was looking through the headline. PSU Bank ended the session in the red on residual nervousness about state-bank exposures, but the loss was small. Private banks, capital goods, and metals were broadly flat to mildly negative. The defensive packs, FMCG and pharma, eked out modest gains as flows rotated into balance-sheet certainty. IT was the day's quiet outperformer, helped by a parallel uptick in the dollar index and a constructive read-across from US tech earnings.

The most striking sectoral move was the absence of one. There was no panic bid into gold-related equities, no flight into government securities, and no spike in the India VIX beyond the high teens. The volatility surface across the broader market re-priced upward by a couple of points and then drifted back down through the following sessions.

The five and ten-session follow-through

By 28 November, five trading sessions after the event, Adani Enterprises had recovered close to half of the 21 November intraday damage, but had not retraced the gap. The 2,400 to 2,500 zone, which had served as support through October, became resistance on the way back up. Adani Ports continued to outperform the rest of the pack and traded back to its pre-event levels within a week. Adani Green remained the laggard and spent the next ten sessions in a slow grind lower as the market digested the procedural risk attached to the US indictment.

The ten-session window, taking the read out to 5 December, was where the verdict became visible. Nifty had stabilised and begun a modest recovery as the FII selling pressure eased and DII buying continued. Bank Nifty led the bounce. Within the Adani pack, the dispersion that opened on the event day widened further. Adani Ports re-rated higher and crossed its pre-event price. Adani Enterprises consolidated in a 2,300 to 2,450 band, waiting for clarity on the indictment proceedings. Adani Green continued to underperform and tested fresh six-month lows by the first week of December.

Brokerage strategy notes published between 22 and 25 November landed in a tighter cluster than one might have expected. The domestic houses argued that the cash flow profile of the listed operating businesses was intact, that the December 2024 maturity wall had been pre-funded, and that the legal process in the US would play out over years rather than weeks. The foreign houses were more cautious on the renewables arm and the unlisted incubation pipeline, but largely concurred that the systemic read-across into Indian banks was limited. Nobody, on either side of the desk, called this a 2023 repeat.

Did the event change the trend, or was it noise?

The honest answer, looking back from 2026, was that 21 November 2024 was noise at the index level and signal at the single-name level. The Nifty trend through November and December was driven far more by the persistent FII outflow, the rupee weakness, and the global rates backdrop than by any one issuer's troubles. The index that registered the event the loudest, the Adani group basket itself, treated it as a re-rating event for the weakest balance sheets in the pack and a non-event for the strongest. Adani Ports closing roughly flat on the day, and trading higher within a week, was the cleanest expression of that distinction.

What changed structurally was the market's willingness to treat the conglomerate as a monolith. Before 21 November 2024, the group stocks moved as a basket on news flow. After, the cash market began to discriminate, and that discrimination held through the calendar-year close. The options market followed, with single-name implied vols on the cleaner entities compressing through December while the laggards held a persistent premium.

For the broader market, the episode was a useful stress test of an architecture that had been built quietly through 2023 and 2024. DII flows had grown deep enough, and bank disclosures clean enough, that a second short-seller broadside on the largest single corporate group did not produce a systemic tremor. That was the durable read.

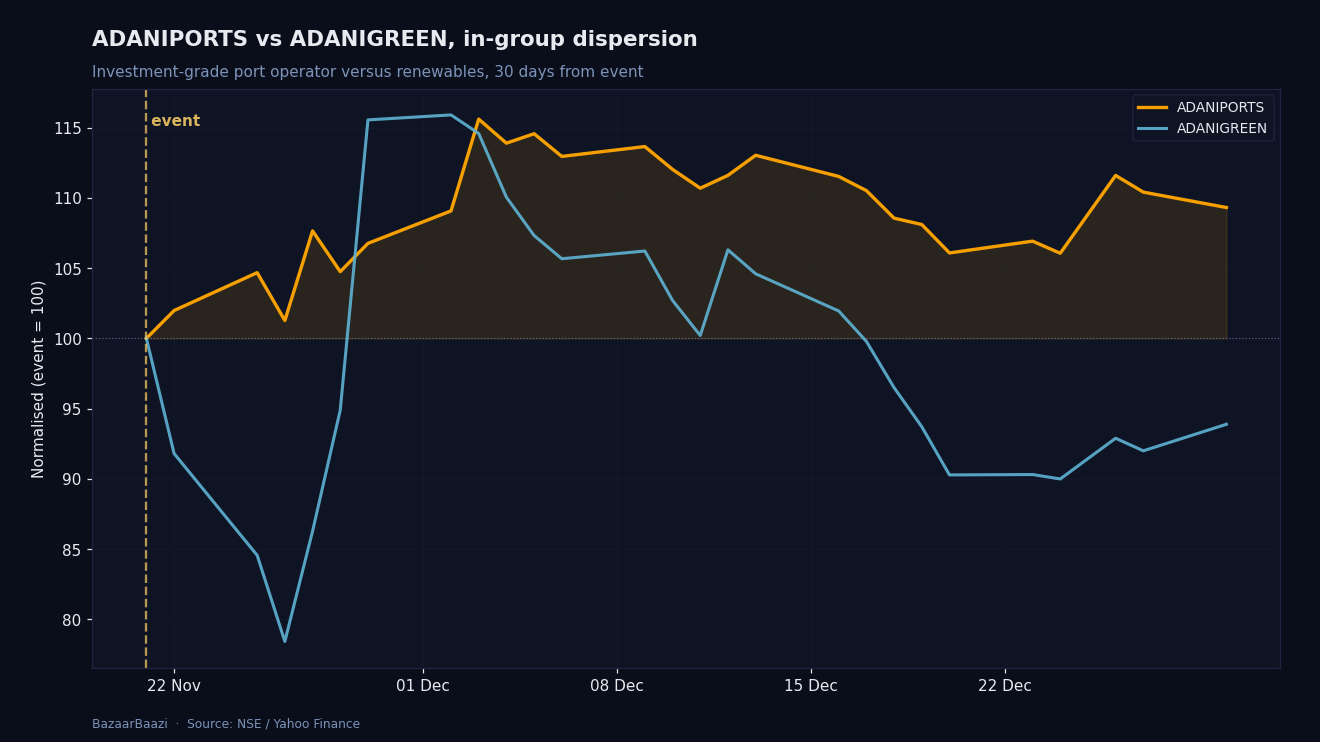

Chart 3, the dispersion verdict. ADANIPORTS closed 21 November at 1,109.25 and re-traced higher to 1,212.60 by 30 December, a gain of 9.32% in the 30-session window. ADANIGREEN, indexed to the same 21 November close of 1,145.70, sank to a 25 November low of 933.00 and finished December at 1,075.65, still 6.11% below the event-day mark. The 15.43 percentage-point gap between the two charts is the dispersion that no headline index could capture.

Verdict

Stance: NEUTRAL on Nifty, BEARISH on the weakest names in the Adani pack, BULLISH on the strongest. Horizon: 1mo to 3mo from the 21 November 2024 event date. Rationale: The cash market correctly priced 21 November 2024 as an issuer-level event with bounded systemic read-across. The intraday reversal in Adani Enterprises and the flat close on Adani Ports established the dispersion trade inside the group basket, and that dispersion was the only Adani-related trade that worked through the subsequent ten sessions. The index itself moved on macro and flow variables, not on the headline.